A recent case serves as a reminder that poorly structured investments can cause unnecessary tax grief. It’s unnecessary because avoiding the grief is relatively straightforward. The case reflects a common scenario such as this:

- You’d like to invest in shares or property

- You want to hold the investments in your family trust

- You have equity in your home

- You borrow from the bank against that equity (or drawn down on your existing home mortgage

- facility that you’ve previously paid down)

- Your trust uses the funds to acquire the investments

Your trust owns the investments and earns the income from them, but it is you personally who has borrowed from the bank. Accordingly, it is you who incurs the interest expense on the loan. Is the interest deductible? Well, that depends on what you do next.

What you have done

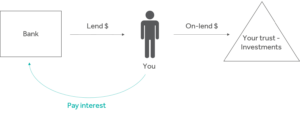

Before getting to that, let’s start by being clear on what you’ve initially done. The bank is not the only lender here – you’ve become one, too. This is what you have really done:

You borrowed from the bank, and then what did you do with the funds? You on-lent them to your trust. Your trust has then used the funds borrowed from you to acquire the investments.

Interest deductible?

Now, back to the question of whether you are entitled to a deduction for the interest you pay to the bank. To cut a long story short, trust us when we say that, if you do nothing further, the answer will be ‘no’. The reason is that there is no direct connection between your interest cost and the trust’s investment income. That will be so even if the trust distributes the investment income to you, and even if the trust commits to distributing all future income to you. The result is an asymmetrical tax outcome – you pay tax on the investment income, but you don’t get a deduction for the interest you pay to the bank.

Recent case highlights the value of getting advice

The above situation is similar to that recent case mentioned at the beginning. The individual was denied a deduction for his interest cost. It’s understood that he did not have any representation, which might explain why he pursued the case, because if he had got some tax advice, it would likely have been that he had no case.

An even better approach would have been to seek advice before undertaking the investment.

Solution

A simple solution to ensure that your interest expense is deductible is to charge interest on your loan to the trust. The interest you pay to the bank now has a direct connection with income you earn – interest received on your loan advanced to the trust. This would result in symmetrical tax outcomes overall:

- Your trust earns the investment income, but the interest it pays to you is deductible in the trust;

- You earn the above interest income, and get a deduction for the interest paid to the bank.

It is important to document in writing the terms of your loan to the trust. There are providers of simple loan agreements for these on-lending situations, via a streamlined online process, that are quick and inexpensive. In addition, demonstrating a profit motive under the on-lend arrangement assists the case for your interest paid to the bank being deductible. This can be achieved by charging the trust an interest rate that is higher than the rate you’re paying to the bank (even if only by 0.1%).

The result is essentially tax neutral for you personally, disclosing interest income and an interest deduction in your tax return. Your trust discloses the investment income and a deduction for the interest paid to you. However, if the investment is negatively geared, the resulting tax loss is locked inside the trust, and can only be deducted against future income in the trust (subject to some integrity rules).

Trade-off

If the investment overall will produce a negatively geared loss in the initial years, and you want to personally claim a deduction, you have to abandon the trust structure, and acquire the investment in your personal name. However, that provides less flexibility when the investment turns income positive and/or is realised for a capital gain. The income/gain is assessed to you, whereas the trust could distribute the income/gain to a beneficiary on a lower tax rate than you.

Acquiring the investment in your personal name or in your trust presents an unavoidable trade-off: tax saving from a deduction now vs greater flexibility later on. There are also non-tax factors in play such as asset protection.

Talk to your trusted Nexia Advisor about structuring investments in the way that works best for you.

Article by David Montani2021