Clients are probably aware of the rules which permit a super fund member to make a non-concessional contribution of up to three times the general non-concessional contributions cap, by bringing forward the non-concessional caps for up to the next two years.

These rules are about to be affected by the indexation of contribution caps and proposed changes to the law.

Due to indexation, these important caps will be changing with effect from 1 July 2021:

These indexation changes will have a significant effect of the tests used to calculate if the non-concessional contributions caps of future years can be brought forward.

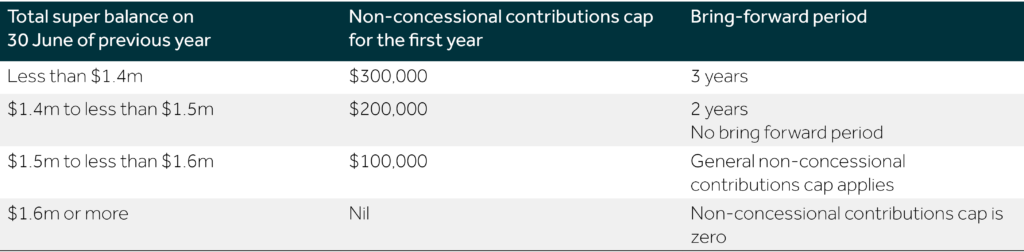

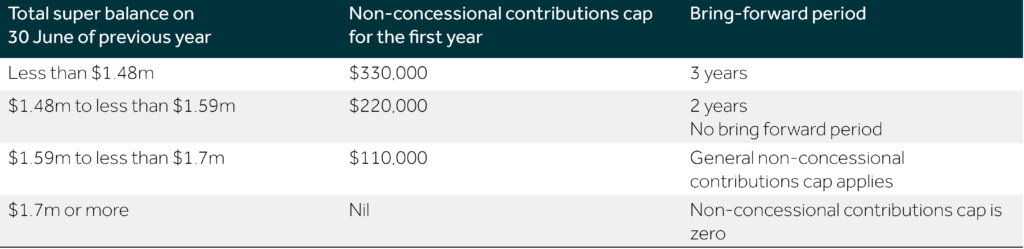

The first test compares the member’s total super balance at the previous 30 June to the general transfer balance cap ($1.6m to 30 June 2021; $1.7m from 1 July 2021) in the year the bring forward is triggered.

The possible situations are:

For your reference, the thresholds outlined above which apply to 30 June 2021 can be summarised in the following table:

They translate into the following table with the indexation of the non-concessional contributions cap from 1 July 2021:

The maximum amount of the brought forward cap is set by reference to the general non-concessional cap applicable in the year the bring forward is triggered. So if you trigger a bring forward on or before 30 June 2021, the increased non-concessional caps which would otherwise apply in 2022 and 2023 are ignored.

There may be situations where two or three years of non-concessional contributions caps are brought forward but the full amount of possible non-concessional contributions is not made in the first year. In this case, the member’s total super balance at the previous 30 June must be measured against the general non-concessional contributions cap in each of the second and third years, and this might rule out making planned contributions in those years. No non-concessional contribution can be made in a year where the member’s total super balance on the previous 30 June is equal to or greater than the general transfer balance cap for that year.

The second test concerns the member’s age. Under the current law, the member must be 65 or younger at some time in the year the bring forward is triggered. The Federal Government has announced its intention to raise this limit to 67, but this is yet to be legislated. A member over 75 is not able to make non-concessional contributions.

The third test concerns the work test. Under the current law, if the member is over 67 at the time of making the contribution, they must meet the work test in that year (or meet the one-year work test exemption). Basically, to meet the work test, a person must be gainfully employed or self-employed for at least 40 hours in a continuous 30 week period during the year.

In the 2021 Federal Budget, the Federal Government announced that the work test is to be abolished for members between 67 and 74 in relation to making non-concessional and salary sacrifice contributions, but this change is not expected to come into effect before 1 July 2022.

Next steps

With these changes, clients should take care in deciding whether to trigger the bring forward before or after 30 June 2021, and whether to use the full brought forward cap in one year. Please contact your Nexia advisor if you have any questions or need any further information or advice.