What happened?

- The less than $20,000 instant asset write-off will be extended to 30 June 2018

- Small business entity threshold has increased to $10 million (was $2 million)

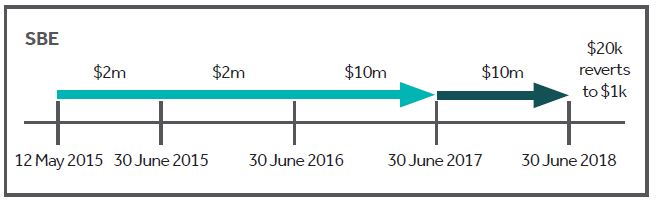

The small business $20,000 instant asset write-off applies from 12 May 2015 to 30 June 2018 (the recent 9 May 2017 budget extended this write-off by another 12 months to 30 June 2018)1 and is available to all small business entities2 (e.g. sole traders, companies, partnerships or trusts).

Under this write-off, small business entities ($10 million threshold for 2017 onwards) will have the benefit of the $20,000 instant asset write-off for most new or second hand depreciating assets bought and used, or installed ready for use, in the business in the 2017 (and now 2018) income tax year.

Small business entities (SBE) that do not choose3 to depreciate their depreciating assets using this small business concession – or businesses that are not SBEs - will have to depreciate their depreciating assets under less favourable depreciation rates under Division 404 of the Income Tax Assessment Act (ITAA 1997).

Instant deduction of taxable purpose proportion

- Only for assets acquired after 12 May 2015

- Deduction in year asset first used / installed ready for use

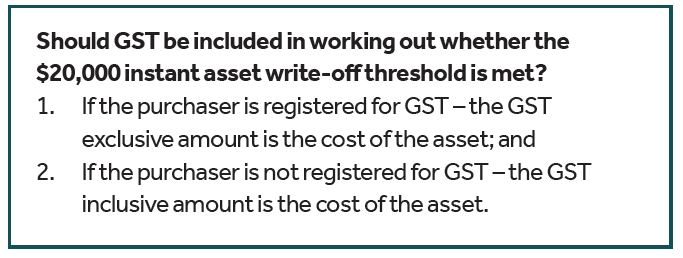

A SBE that acquires business assets (e.g. cars, vans, machinery or kitchen equipment) for less than $20,000 (on a cost per asset basis) for the first time after 12 May 2015, may write-off the business use proportion of an asset in the income tax year in which the asset was first acquired and used or installed ready for use.

Therefore, assuming a SBE buys a $22,000 machine which is only used 80% of the time in the business, the $20,000 instant asset write-off would not be available even though the business use proportion would be only $17,600 ($22,000 x 80%). The $17,600 business use proportion amount will be included in the general small business (depreciation) pool and depreciated accordingly (see below).

An immediate deduction is available for amounts less than $20,000 spent on improving or transporting a depreciating asset5 (provided such costs are incurred between 12 May 2015 and 30 June 2018).

1. What about business assets costing $20,000 or more?

-

Irrelevant when asset was first acquired

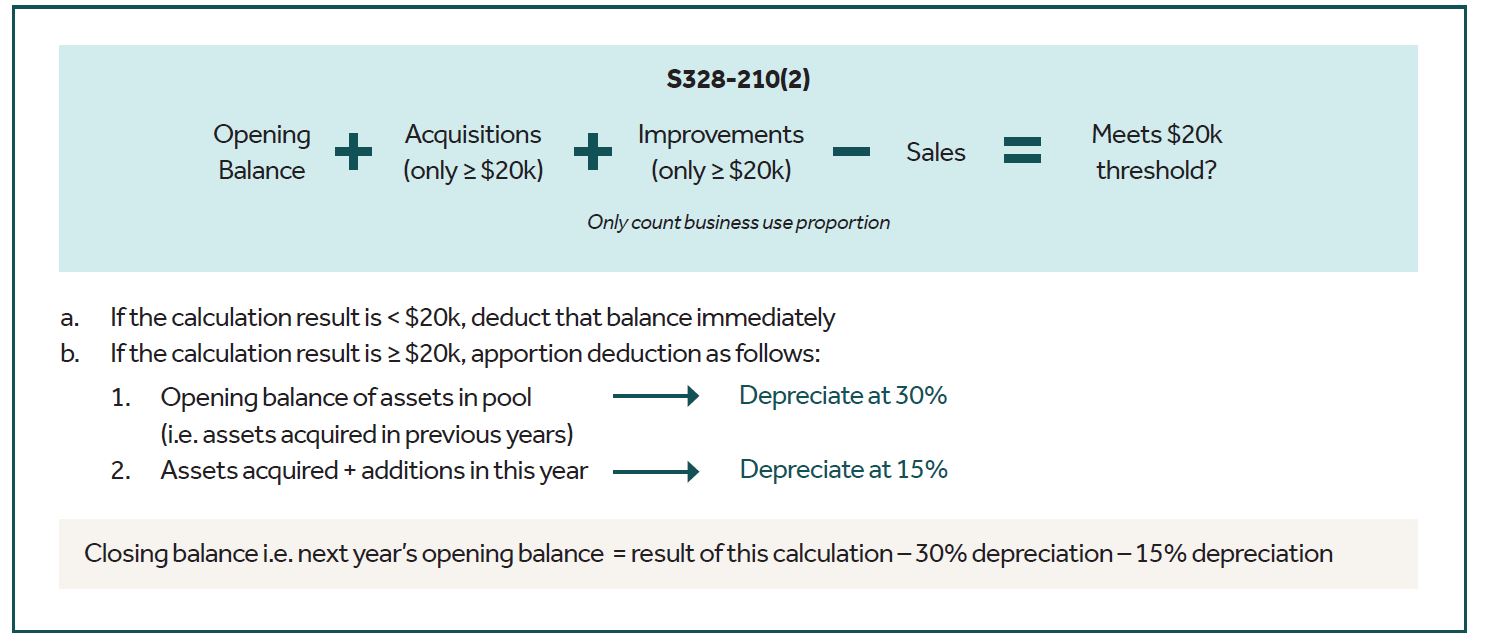

Assets costing $20,000 or more do not qualify for this immediate deduction – instead, the whole amount will form part of the general small business depreciation pool.

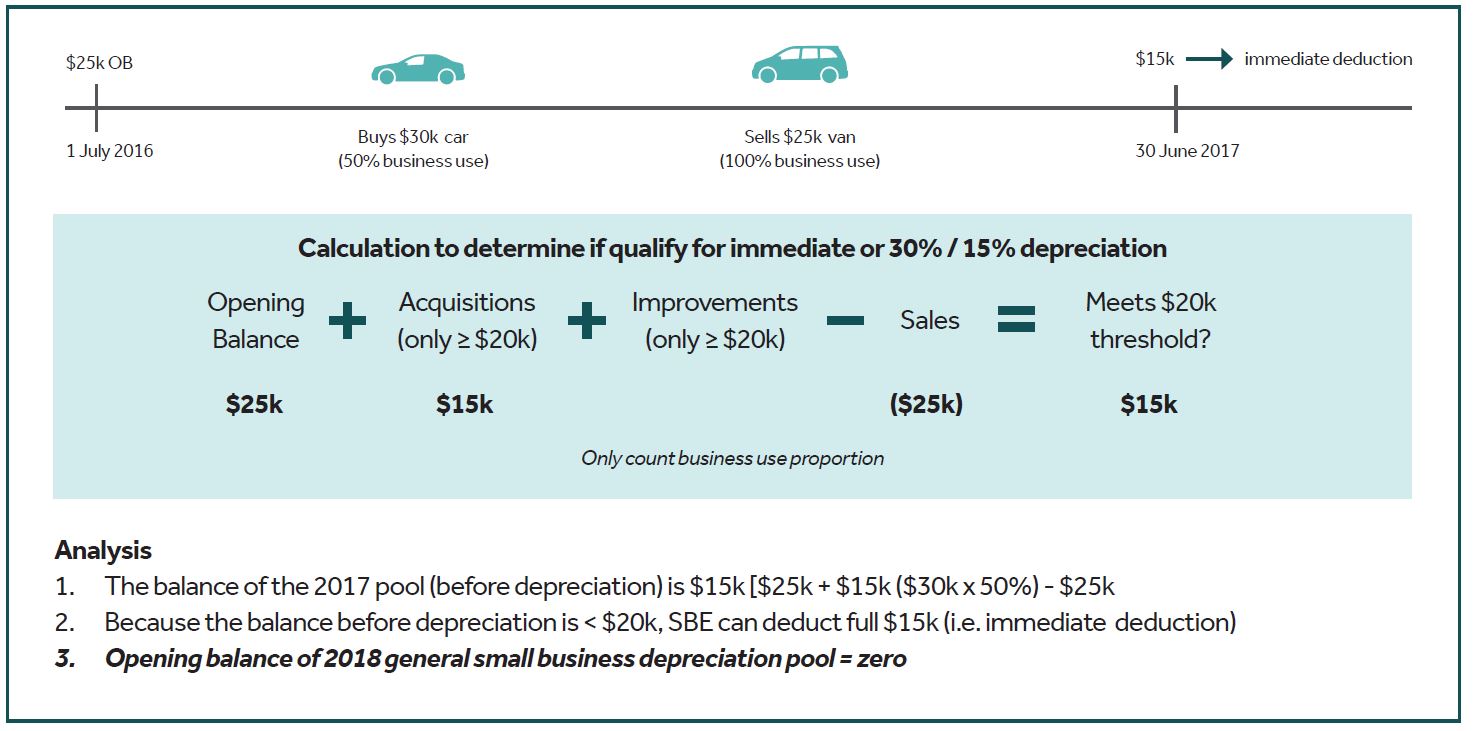

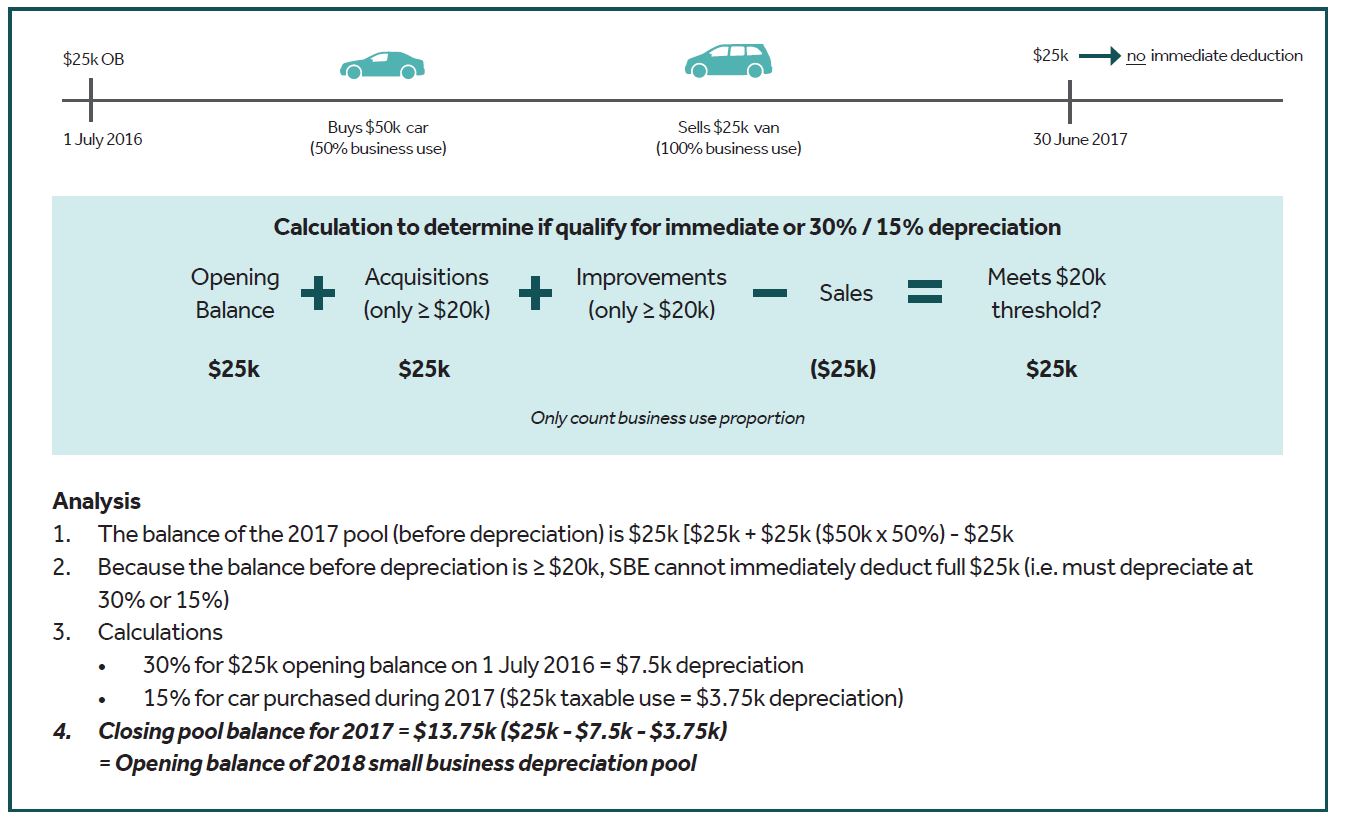

The diagram below sets out a methodology to apply when depreciating assets in the general small business depreciation pool for the following two practical examples:

(A) Immediate deduction because calculation result (i.e. balance before depreciation) < $20,000

(B) 30% / 15% depreciation because calculation result (i.e. balance before depreciation) ≥ $20,000

Therefore, if the closing balance of the pool (before depreciation) is $20,000 or more, the taxable purpose proportion will be depreciated:

- at 15% in the first income year (i.e. for assets acquired and additions in the current year);

- at 30% each income year after that (i.e. the opening balance of assets in the pool).

Once the closing balance of this pool falls below $20,000, the balance can be immediately deducted in that year (regardless of when the assets were purchased6).

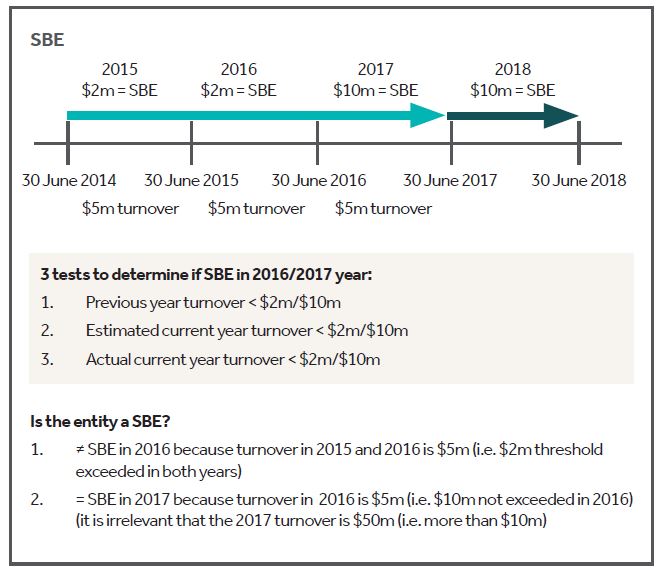

Effect of the Small business entity threshold increase to $10 million

As the timeline below illustrates, the SBE threshold has increased to $10 million from 1 July 2016 onwards.7

(1) Effect on the test for a small business entity

From 1 July 2016, a business will be a SBE if a business is carried on in the current year and was either carrying on a business in the previous year where its aggregated turnover was less than $10 million or its aggregated turnover for the current year is less than $10 million – the aggregated turnover is determined on either a prospective basis at the beginning of the year or a retrospective basis at the end of the year.

The interaction of the SBE threshold change as well as the 3 different SBE tests can produce some interesting results.

The example below illustrates that:

- an entity with a turnover of $5 million in both the 2015 and 2016 income tax years will not be a SBE in the 2016 income tax year; and

- and entity with a turnover of $5 million in the 2016 income tax year but a turnover of $50 million in the 2017 income tax year will be a SBE in the 2017 income tax year because the entity’s turnover in 2016 was less than $10 million.

(2) Effect on the general small business depreciation pool

Following on from the example above, because the entity will not be a SBE in 2016 (because the $5 million turnover is more than the 2016 SBE threshold of $2 million), the $20,000 instant asset write-off (for purchases less than $20,000) and small business depreciation pooling rates (for purchases of $20,000 or more) will not be available in 2016. The normal Division 40 depreciation rules will apply in 2016 because the entity will not be a SBE in 2016.

However, because the entity will be a SBE in 2017 (because the $5 million turnover in 2016 is less than the 2017 SBE threshold of $10 million) the instant asset write-off and small business depreciation pooling rates should be available for the SBE in the 2017 income tax year8.

Practically this will mean that in the 2017 income tax year, the SBE can choose9:

1. for assets used for the first time (or installed ready for use) in 2017 (i.e. when the entity is a SBE):

- to claim the instant asset write-off if the asset cost less than $20,000; or

- to depreciate assets costing $20,000 or more in the small business depreciation pool; and

2. for assets used for the first time (or installed ready for use) in 2016 (i.e. when the entity was not a SBE):

- to make the closing balance / adjustable value10 / written down value of the Division 40 depreciation items (with certain exceptions)11, to be the opening balance of the 2017 small business depreciation pool and depreciate that balance at 30%12 (provided the balance of the 2017 small business depreciation pool – before depreciation - is $20,000 or more)13.

The choice to use the accelerated small business depreciation (i.e. the $20,000 instant asset write-off and simplified small business depreciation pools) will be evidenced by the way the taxpayer claims depreciation deductions in the taxpayer’s tax return (i.e. whether deductions are claimed under the normal Division 40 depreciation provisions or the specific SBE depreciation provisions).

How can Nexia help you?

These small business tax measures generate immediate tax savings and hopefully will stimulate the economy.

In particular, the $20,000 instant asset write-off is very business friendly – not only because the previous instant write-off cap was only $1,000 – but also because this instant asset write-off also applies to second-hand asset purchases and the $20,000 limit is on a per asset basis (i.e. you can buy as many similar business assets as you want in the relevant time).

However, Treasury has warned that that they are checking assets acquired under artificial or contrived arrangements (e.g. where a number of related SBEs sell their assets to one another and write off the full value of those assets under the increased threshold).

We would be happy to assist you with your depreciation claims on any business assets you may have acquired – to ensure you gain the maximum deduction possible.

With the increase of the SBE threshold to $10 million from the 2017 income tax year, additional opportunities exist for entities with turnovers between $2 million and $10 million.

Please speak to your local Nexia Tax Adviser if you would like to know more about how these small business measures may assist your business.

1 - The Treasury Laws Amendment (Accelerated Depreciation for small business entities) Act 2017 received Royal Assent on 22 June 2017.

2 - Including those who previously opted out of the accelerated small business depreciation rules (See paragraph 1.2 and 1.9 of the Explanatory Memorandum to the Treasury Laws Amendment (Accelerated Depreciation for small business entities) Act 2017

3 - S328-175 of the ITAA 1997.

4 - Depreciating assets that are capital works (e.g. buildings and structural improvements), cars using the cents per kilometre method for calculating car expenses and other depreciating assets for which deductions are available under other specific provisions outside Division 40 (e.g. film provisions) cannot be depreciated under Division 40 or the small business depreciation concessions.

5 - Second element of the cost base of depreciating assets

6 - Paragraph 1.26 Example 4 of the Explanatory Memorandum to the Tax Laws Amendment (Small Business Measures No. 2) Act 2015 contains an example where the $20,000 instant asset write-off is available for assets bought before 12 May 2015 that have depreciated to below $20,000 in the general small business depreciation pool.

7 - The Treasury Laws Amendment (Enterprise Tax Plan) Act 2016 received Royal Assent on 19 May 2017.

8 - According to paragraph 2.4 of the Explanatory Memorandum to the Treasury Laws Amendment (Accelerated Depreciation for small business entities) Act 2017, “Businesses with a turnover between $2 million and $10 million gain access to the concession from 1 July 2016 under the Enterprise Tax Plan legislation.”

9 - Pursuant to s328-175(1) of the Income Tax Assessment Act 1997 (ITAA 1997), a small business entity must choose to depreciate assets under the capital allowances available for small businesses (Subdivision 328-D).

10 - The adjustable value of a depreciating asset at the end of the year is the depreciating asset’s cost reduced by any decline in value up to that time.

11 - Note that Division 40 provides specific rules for working out deductions for different kinds of assets (e.g. immediate deduction for certain non-business depreciating assets costing $300 or less, certain low value and software development pools, primary production depreciating assets and capital expenditure that is either immediately deductible or deductible over time). Horticultural plants, assets predominantly let on depreciating asset leases, assets in a low value pools or in software development pools and assets qualifying for research and development (R&D) relief cannot be depreciated under the small business depreciation concessions (s328-175 of the ITAA 1997).

12 - S328-220(2) of the ITAA 1997

13 - As illustrated in Example 1B above.