Let us help you with your extra tax compliance obligations

As part of a global Organisation for Economic Co-operation and Development (OECD) initiative to prevent profit-shifting and revenue leakage, Australia has enacted various new laws aimed at strengthening Australia’s transfer pricing regime. Multinationals operating in Australia should be aware of these tough new measures to properly manage their risk exposure to Australian (and worldwide) taxes.

Because these changes will impact significant global entities (SGEs) – broadly an Australian entity will be a SGE if the Australian entity is part of a multinational group (consolidated for accounting purposes) and the group has annual global income of $1 billion (AUD)1 or more – it is incumbent on such SGEs to familiarise themselves with these additional compliance obligations that apply to them.

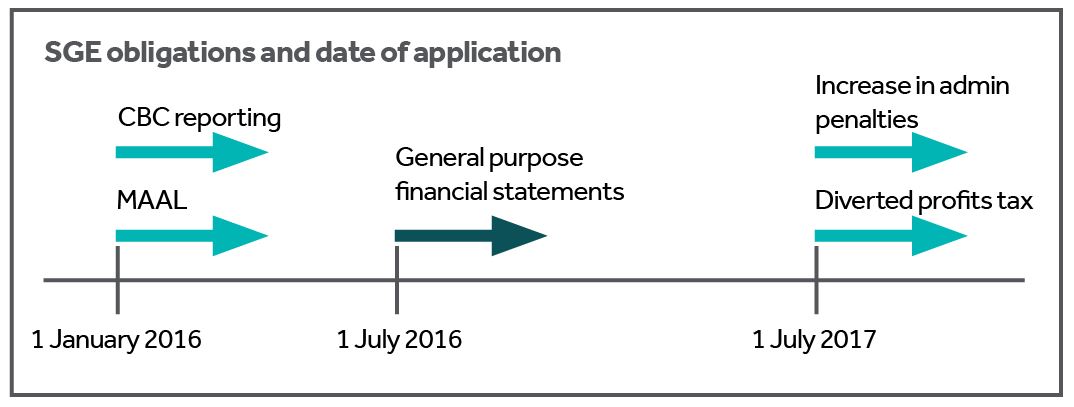

The timeline below illustrates the start dates of these additional obligations that are imposed on SGEs.

SGEs that do not comply with their obligations will face severe administrative penalties2:

- penalties for failure to lodge tax documents on time has increased by 100 times [i.e. a simple late lodgement of any tax document can lead to a penalty of $105,000 (if late by 1 day) to $525,000 (if more than 16 weeks late)]; and

- penalties for failure to take reasonable care when determining tax liabilities have doubled (i.e. $25,200 for intentional disregard, $16,800 for recklessness and $8,400 for failure to take reasonable care when applying the tax law).

To prevent these extreme penalties, SGEs should therefore ensure that they satisfy all these new obligations and lodge the relevant documents on time.

Set out below are some questions and comments aimed to make the reader aware of some risks SGEs may encounter as they progress through the SGE obstacle course of compliance obligations and tax consequences.

1. Is the entity a significant global entity and therefore affected by these rules?

Because these additional rules apply to SGEs, we would encourage Australian entities that are part of large multinational groups to come and talk to us so that we can determine whether the entity would be a SGE and therefore subject to these rules.

Note, the Australian entity may be a SGE even if the Australian entity has negligible income in Australia but the global income of the multinational is at least $1 billion (AUD) in the year.

2. An Australian taxpayer that is a SGE will be subject to these additional compliance obligations

In particular, the Australian taxpayer will have to disclose in its tax return whether it is a SGE.

Provided the Australian entity is a SGE, the Australian entity (and not the foreign head company3) may have to lodge:

- general purpose financial statements (i.e. Tier 1 general purpose financial statements or Tier 2 Reduced Disclosure Regime (RDR) financial statements, as applicable) with the ATO (if they do not lodge such statements with ASIC) ;

- transfer pricing documentation (e.g. country-by-country (CBC)6 reports such as local files7) with the ATO within 12 months after the end of each income year.

Therefore, SGEs with substituted accounting periods of 31 December 2016 will have to lodge these CBC reports by 31 December 2017.

If either the general purpose financial statements or CBC report is lodged late, significant penalties could apply (see above).

Australian taxpayers that are part of multinational groups should have conversations with their foreign head entities about what information they will need to collate for local CBC reporting.

3. An Australian taxpayer that is a SGE will be subject to these additional tax consequences

(a) Multinational anti-avoidance Law (MAAL)8

Broadly, the MAAL aims to prevent multinationals from contriving to not have a taxable presence / permanent establishment (PE) in Australia and therefore attempting to book profits from Australian sales to overseas low tax jurisdictions (and not pay tax in Australia).

If the MAAL applies, the ATO can attribute such income to the Australian entity, make the income subject to Australian tax and impose increased administrative penalties (see above).

(b) Diverted profits tax (DPT)9

Broadly, the DPT is a penalty tax of 40% on the profits that have been diverted to significantly lower tax jurisdictions (e.g. broadly foreign countries with a company tax rate that is less than 80% of the tax rate in Australia ).

An Australian taxpayer with income of less than $25 million may also be exempt from the DPT.

The way forward

These requirements are very complex and place a substantial burden on such multinationals to comply with the Australian rules.

Since Nexia is a global accountancy network with offices all over the world, we are well-equipped to handle multinational tax and disclosure issues.

Please contact us so that we can assist you in complying with these obligations and to help you manage your exposure to risk.

1 - Unless otherwise specified, all currencies are expressed in Australian dollar (AUD).

2 - Increase in administrative penalties applies from 1 July 2017

3 - A foreign head company may have to lodge a global CBC report (showing the global activities of the multinational as well as the location of its income and taxes paid) in the foreign jurisdiction. The ATO may obtain a copy of this report from the foreign revenue authority through exchange of information provisions.

4 - The obligation to lodge general purpose financial statements applies for years beginning on or after 1 July 2016

5 - Failure to lodge these general purpose financial statements will also lead to increased administrative penalties (see above).

6 - CBC reporting applies to years commencing on or after 1 January 2016

7 - The Local File provides detailed information on the specific intercompany related party dealings relevant to Australia.

8 - The MAAL applies from 1 January 2016

9 - DPT applies from 1 July 2017

10 - s177L of the Income Tax Assessment Act 1997. Australian businesses diverting profits to Singapore, Hong Kong, UK and Ireland may be subject to DPT because these countries have tax rates of lower than 24%.