What happened?

Large businesses must disclose their most contestable and material tax positions on a reportable tax position (RTP) schedule that has to be lodged together with their company tax return1.

Businesses that have already engaged with the ATO regarding uncertain tax positions [e.g. entering into Annual compliance agreements (ACAs)2, Advanced Pricing Arrangements (APAs)3, Pre-lodgement Compliance Reviews (PCRs), Streamlined Assurance Reviews (SARs) or applied for private rulings on tax issues they are not sure of], will not be required to fill in the RTP schedule. A taxpayer may also make an early disclosure of an RTP - and if this early disclosure form is received by the ATO at least 28 days before the taxpayer is due to lodge the taxpayer’s company tax return – such an uncertain tax position does not need to be disclosed on the RTP schedule.

The ATO uses the RTP schedule disclosures to help focus their compliance activities and identify areas in the tax law that may need clarification, legislative improvements or further advice and guidance.

Currently, not many large companies have to lodge a reportable tax position (RTP) schedule (in 2013 only the largest 170 taxpayers had to lodge RTPs).

However, from the 2018 income tax year onwards (e.g. for income years ending on or after 30 June 2018 or SAP income years ending on or after 31 December 20174), companies in economic groups with turnover greater than $250 million will also have to lodge RTP schedules. Roughly, this means that the top 1,000 companies will have to lodge RTP schedules.

The ATO will notify taxpayers in advance whether they will need to lodge a RTP schedule.

Although a disclosure in a RTP schedule will not constitute a voluntary disclosure, the way a RTP is completed may lead to a remission of penalties (e.g. where the information provided in the RTP schedule is sufficient for the ATO to identify and calculate any tax shortfall amount).

What does this mean for you?

1. When does an RTP have to be disclosed?

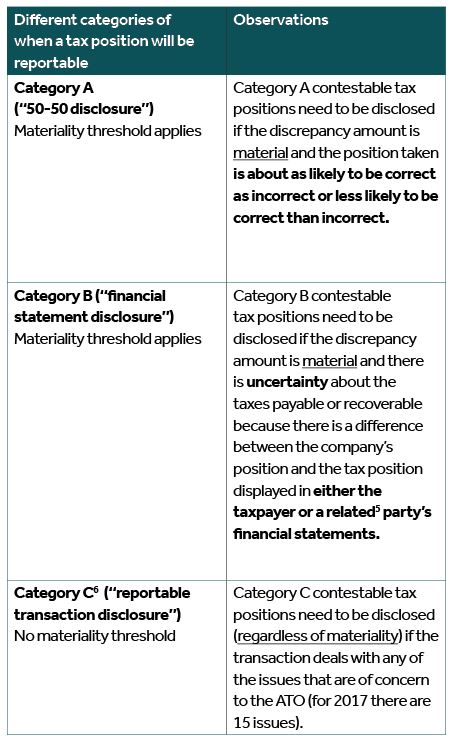

A tax position taken on a company tax return (i.e. as evidenced by the way the company tax return was filled in) will be contestable if such a position falls into one of the RTP categories (or a combination of the categories) set out in the table below:

Category A tax positions will not be contestable (and therefore will not have to be disclosed) if the taxpayer exercised reasonable care (i.e. by consulting authorities) when completing the tax return and the conclusions drawn are more likely to be correct than incorrect7.

A typical example of a Category B tax position would be where the tax disclosures made in financial statements of overseas related parties are materially different from the taxation treatment adopted in Australia.

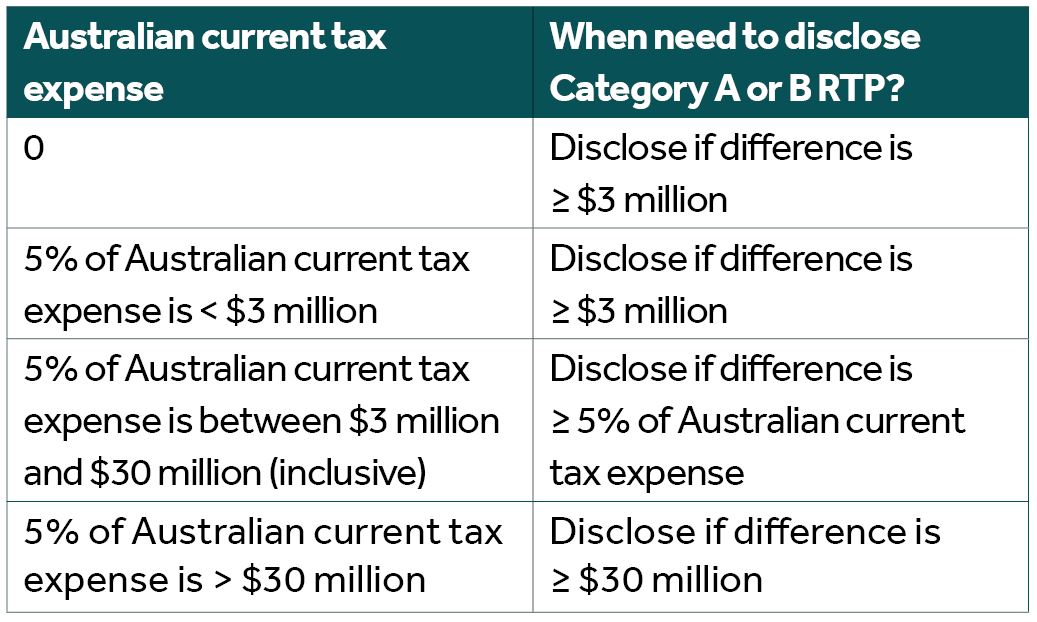

There is also no need to disclose Category A or Category B tax positions if the amounts involved are not material. As the table below illustrates, materiality (and when to disclose a contestable Category A or Category B position) depends on the size of the difference between the taxpayer’s position and the ATO’s position regarding current tax expense.

Because Category C tax positions basically comprise the latest tax arrangements identified by the ATO (e.g. for the 2017 RTP there are 15 questions dealing with the latest tax issues the ATO finds disconcerting as evidenced in recent taxpayer alerts, public rulings and cases), a taxpayer will have to disclose their involvement in such arrangements (regardless of any materiality threshold).

2. How does the disclosure process work?

When disclosing RTPs, a taxpayer must fill in the RTP schedule outlining the following (in 500 words or less – but can attach more information if necessary):

- A concise description of the relevant facts, circumstances, arrangements and transactions explaining the RTP;

- A basis for the position taken in the income tax return (i.e. the relevant authorities and any industry or administrative practices such as anti-avoidance rules, integrity provisions, transfer pricing and market valuations);

- Details of a related party involved (if any); and

- The type of position involved (e.g. a Category A, B, or C RTP).

Common areas that are often disclosed on the RTP schedule include:

- Whether the Research & development tax offset can be claimed;

- Whether the transfer pricing rules apply to a taxpayer’s circumstances; and

- Material positions in relation to claiming tax losses.

3. What happens if a company gets the RTP disclosure wrong?

Administrative penalties will apply:

- for false and misleading statements [e.g. $10,800 for intentional disregard, $7,200 for recklessness or $3,600 for failure to take reasonable care – for SGEs, these penalties have doubled)]; or

- if the RTP schedule is not lodged on time [e.g. $1,050 (if late by one day) to $5,250 (if late by more than 112 days) – for significant global entities (SGEs) these penalties increase 100-fold].

How can Nexia help you

Since the introduction of RTP reporting as a pilot scheme back in 2011, RTP reporting, coupled with other real-time compliance offerings such as ACAs, APAs, PCRs and SARs have become part of how the ATO manages risk in the large market.

With these ongoing pre and post lodgement assurance tools supporting the “prevention is better than cure” mantra, being tax transparent has become a new “badge of honour” for taxpayers.

Therefore, it is important for taxpayers to ensure they have an appropriate tax risk management policy in place to adequately identify when and whether a tax position will need to be disclosed and when there will be no need for disclosure (e.g. for Category A tax positions, no disclosure will be necessary if the tax position is more likely to be correct than incorrect).

Please contact us if you have been notified by the ATO to complete a RTP schedule. It is very important to seek professional advice immediately in such circumstances.

Nexia Australia has the necessary experience in dealing with the ATO and assisting you in completing the RTP schedule to ensure you get the outcome that is best for you in your circumstances.

1- A taxpayer can also disclose a reportable tax position before lodging their company tax return by filling in an RTP early disclosure form.

2 - ACAs are administrative arrangements available for all kind of taxes (e.g. income tax, GST and FBT) which a large taxpayer can enter into with the ATO to decrease the taxpayer’s risk profile. The purpose of entering into an ACA is to identify tax issues early to avoid costly audits, reviews and tax disputes. An ACA can provide practical certainty – through issuing “sign-off letters” – that a tax return for a particular year is closed from further review or audit.

3 - An APA is an arrangement that determines in advance an appropriate set of criteria (e.g. method, comparables and appropriate adjustments) to determine the transfer pricing of transactions. (Paragraph 2 of PS LA 2015/4)

4 - Where a SAP ends on any date between 1 December and 31 May the period adopted is in lieu of the income year ending on the succeeding 30 June (Paragraph 4A of PS LA 2007/21)

5 - Whether a party is related is determined by accounting (and not tax) principles.

6 - Examples of Category C reportable transactions include claiming deductions in relation to non-assessable non-exempt (NANE) income, funding dividends or share buy backs through equity raising, using procurement or marketing hubs, treatment of internally generated or revalued intangible assets for thin capitalisation purposes, restructuring of significant global entities (SGEs), financing through cross currency interest rate swaps, cross-border leasing arrangements of mobile assets, permanent establishments (PEs) of consolidated groups, cross-border round robin type arrangements and related party debt funding, research and development (R&D) and exploration expenditure arrangements.

7 - Paragraph 35 of MT 2008/2