This alert is very relevant for you if you are a primary producer (e.g. involved in farming activities)

What happened?

Following on from the Government’s 2015 Agricultural Competitiveness White Paper1, the Government recently released a Bill2 that will make farm management deposit (FMD) schemes more attractive for farmers3 to invest in.

In short, from 1 July 2016:

-

There will be a new cap of $800,000 that can be held in FMDs by farmers (the cap is currently $400,000);

-

Some drought affected farmers may access their funds held in FMDs at an earlier time without incurring penalties; and

-

Some amounts held in FMDs may offset a loan or other debt – resulting in lower interest being charged on the original loan (and if the other loan does not relate to primary production activities there can be administrative penalties).

-

Increase lifetime FMD cap to $800k (was $400k)

-

Early release for drought affected farmers

-

Allow funds held in FMDs to act as offset against other farming loans

This alert will explore what these proposals practically mean for you and what bene ts they may hold for your primary production business / farming activities.

What do these 3 FMD proposals practically mean for you?

1. Increase in FMD cap to $800,000 (currently $400,000)

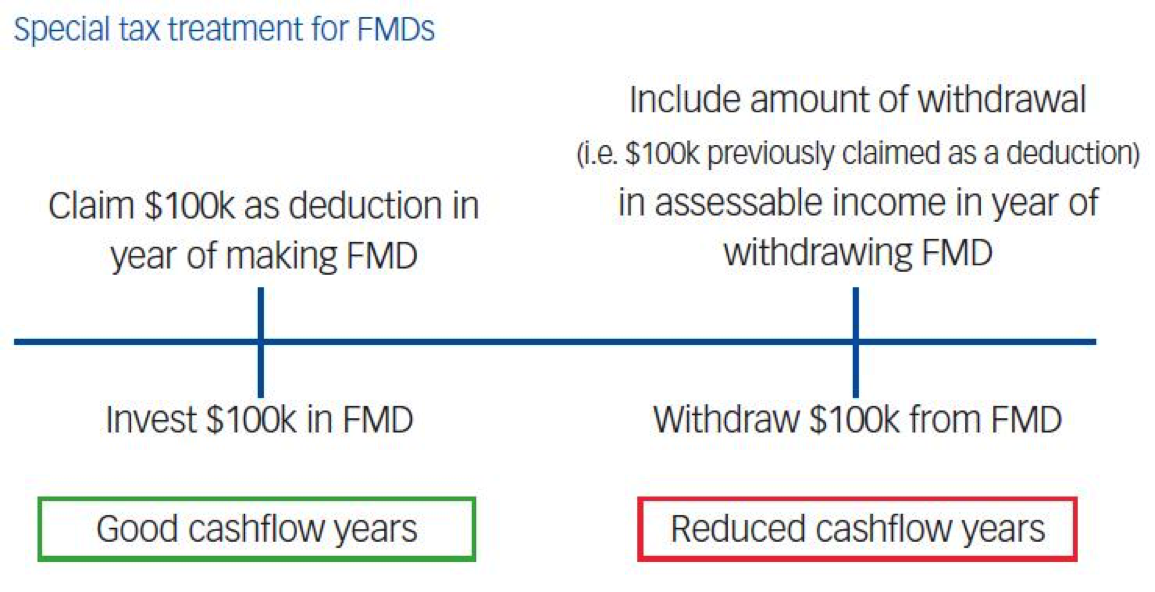

As you may be aware, through investing in FMDs, individuals carrying on a farming business (including a farming business an individual carries on as a partner in partnership or as a beneficiary of a trust) are provided with a tax holiday.

In broad terms this means that if such a FMD investment is held for more than a year, such farmers may claim deductions for amounts deposited in the year deposits are made and only include the amount of such deductions claimed in their assessable income in the year they withdraw these deposits.

By increasing the maximum amount that may be invested in FMDs from $400,000 to $800,000, there is now more potential for farmers to improve their cash flow in this way (i.e. because they can claim an upfront deduction and recoupment of the tax deduction only occurs in a later year).

Note that any amounts contributed in excess of this new $800,000 cap will not be a FMD (and thus not qualify for a deduction in the year of contribution)4.

2. Early release for drought affected farmers

-

Broadly, this measure allows farmers to deposit funds (up to the $800k cap) in FMDs with confidence knowing that if they experience severe drought and need to withdraw monies so deposited within 12 months, they can safely do so without losing access to the previously claimed tax deduction.

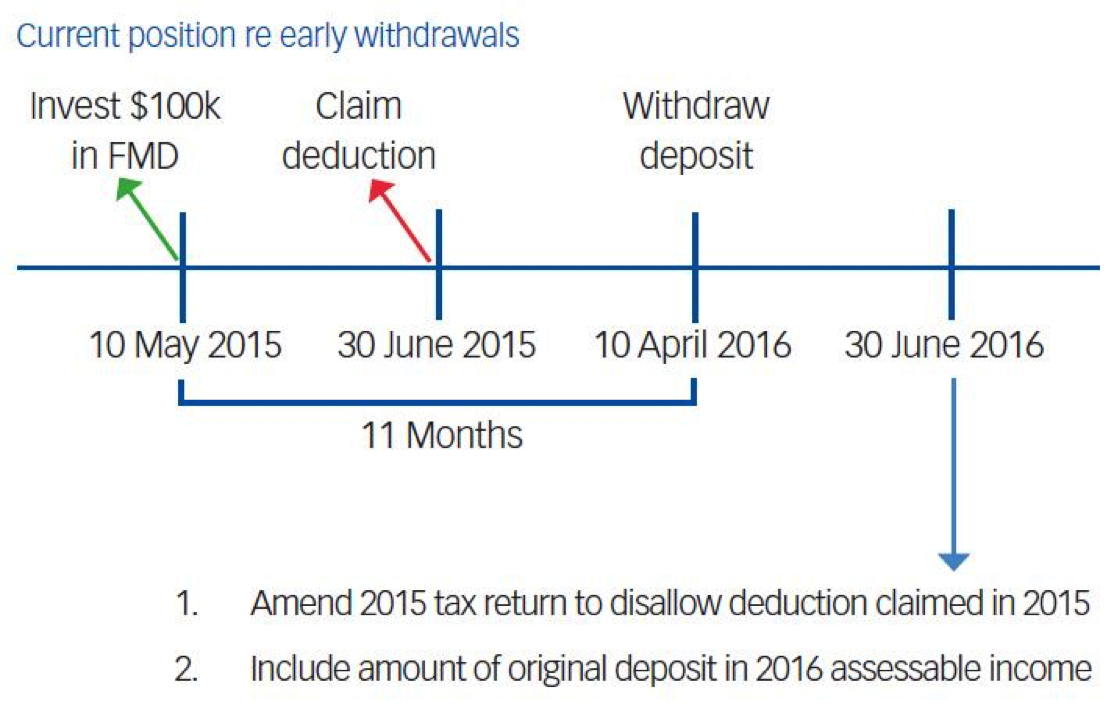

Currently, when farmers withdraw their deposits from FMDs within 12 months of making such a deposit, they will:

-

have to amend their previous year’s income tax return to remove the deduction claimed for the amount originally deposited in the FMD; but

-

still include the amount of original deposit in their assessable income in the year of withdrawal.

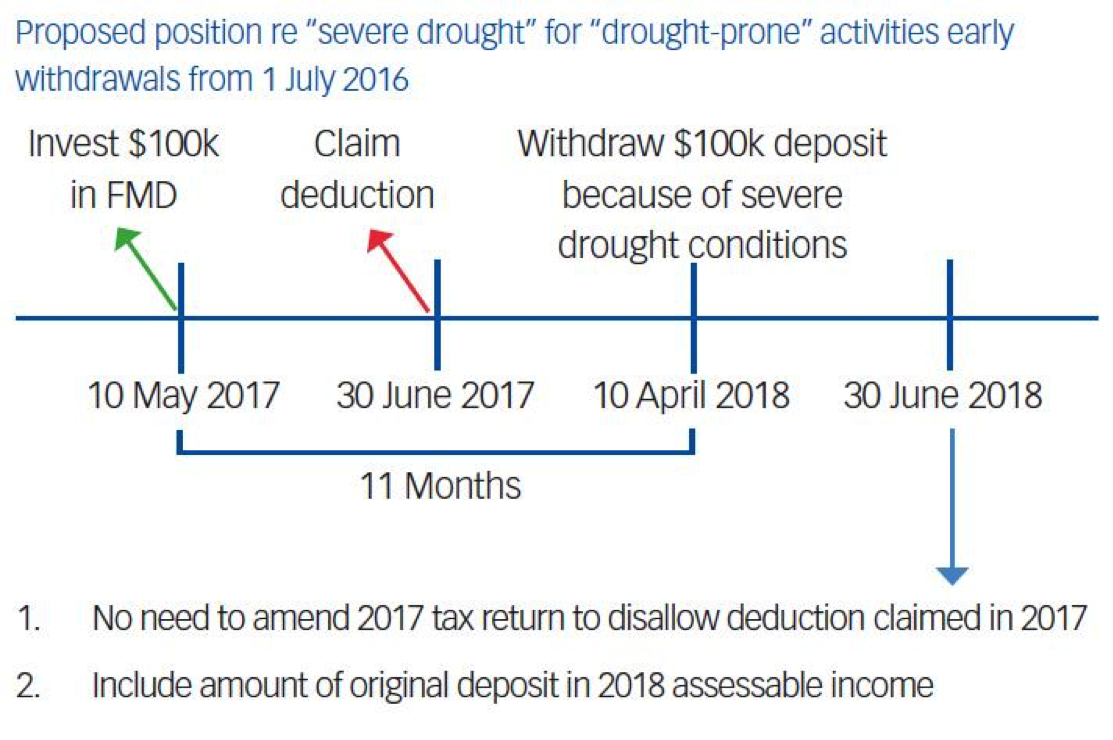

However, from 1 July 2016, it is proposed that some “drought- prone5” farmers experiencing severe drought conditions (de ned opposite) would be able to make such withdrawals within 12 months of making the deposit – without any adverse tax consequences.

This means that for such post 1 July 2016 contributions, they will:

-

still be entitled to the original deduction claimed on contribution to the FMD (and would therefore not need to amend their previous year’s tax return to deny such a deduction); and

-

still include the amount of the original deposit in their assessable income in the year of the withdrawal.

What are severe drought conditions?

Such qualifying farmers will have severe drought conditions if they can demonstrate that at least a part of the land (on which “drought-prone” farming activities have been carried on) has experienced a rainfall deficiency for at least 6 consecutive months (i.e. rainfall ≤ 5% of the average rainfall for that 6 month period based on Bureau of Meteorology (BOM) statistics) or any other conditions that future regulations may prescribe. This 6 month requirement necessarily means that the amount withdrawn cannot be withdrawn within 6 months of depositing it as a FMD.

It is refreshing that a farmer may self-assess (based on publicly available BOM information) whether it meets the conditions for early release (i.e. whether there is severe drought conditions) – there is no need to apply to any Government agency to exercise discretion before funds can be released early6.

This “severe drought” concession will not be available for amounts deposited and withdrawn in the same income year. If this were to happen, the net tax effect would be zero – i.e. the amount of the withdrawal will be assessable in the same year that the amount of the contribution would be allowed as a deduction.

3. FMD funds can be used as an offset account (to set off against interest on other farming loans)

- This concession only applies in relation to loans held by an individual either as sole trader or as partner in a partnership (i.e. not for loans held through trusts carrying on a farming business).

This new concession allows funds held in FMDs to be used as an offset account (to set off against other interest payable on other farming loans the FMD holder may have). Such other farming loans can include secured or unsecured loans, loans with redraw facilities, bank overdrafts and lines of credit in respect of a primary production business carried on either directly as a sole trader or through a partnership7 (not for loans through a trust).

Note however that if such funds in the FMDs are used to offset the amount of interest payable on non-primary production / farming loans, an administrative penalty of 200% of the amount by which the interest has been reduced, will apply. However, the Commissioner has a discretion to remit this penalty.

It is therefore advisable to keep separate loan accounts to distinguish each type of loan (i.e. those loans that are for primary production / farming purposes and those that are not).

How can Nexia help you?

- Contact us if you are involved in farming activities – we would love to talk to you about how these incentives may help your business.

Nexia recognises that farming forms the backbone of Australian society. Therefore we are pleased that the Government is working on ways to improve the way the tax system operates for primary producers / farmers and granting them easier access to finances if there is a drought.

We believe that these measures are a good first step in assisting farmers to manage seasonal and extended periods of fluctuations in cash ow (as are often experienced by farmers).

If you are involved in farming and are interested in exploring possible ways that these new incentives may be of value to you, we would be pleased to hear from you.

Our team at Nexia Australia has considerable farming experience and we are looking forward to assist you further with all your farming business needs.

Please contact your Nexia Advisor so that we can start a conversation / continue the conversation about how we can help you create more value for yourself and your farming business.

1 - Released on 4 July 2015.

2 - Tax and Superannuation Laws Amendment (2016 Measures No 1) Bill 2016 introduced into Parliament on 10 February 2016.

3 - The legislation uses the concept of primary production business that basically refers to someone who is involved in farming activities (see s995-1 of the Income Tax Assessment Act 1997). These concepts are used interchangeably throughout the alert.

4 - Ss 393-30(3) and 393-5 of the ITAA 1997

5 - Farming activities that would be most affected by severe drought - for example, farmers involved in vegetable cropping, cattle farming and dairy farmers – as opposed to farmers involved in commercial shing, felling of trees or transporting trees - that will most likely not be affected by severe drought.

6 - Previous guises of the FMD legislation contained an “exceptional circumstances” provision where funds could only be withdrawn early if a Government agency made a determination that the primary producer would in fact qualify for such exceptional circumstances of early release.

7 - Proposed ss 393-25(3) & 393-37.