It was a simpler time. Your business made a profit, paid 30% company tax. You then extracted the remaining 70% as a dividend when it suited, and you paid the balance of tax up to your personal rate. But now, things aren’t so simple. And, surprise-surprise, it could cost you more tax.

Nostalgia isn’t what it used to be

But first, let’s finish the nostalgia trip with the above dividend. If you were on the top personal tax rate of 47%, you simply paid the balance of 17% (known as “top-up” tax). That left you with 53% of your business profit, reflecting tax borne at your personal rate.1 That’s our dividend imputation system at work, where the tax paid by a company is attached to a dividend as a credit (“franked”). It prevents double-taxation on business profits for Australians, and is a very sensible system.

Lower company tax rate, but…

Our double-taxation-preventing imputation system has unfortunately become a little less preventative. The reason, paradoxically, is the reduction in the company tax rate for small and medium businesses. From 30% a few years ago, it has fallen in several stages, and now from 1 July 2020 is 26% where group-wide turnover is below $50 million and no more than 80% of the company’s income is passive income. All other companies continue with a 30% rate.

Here’s the thing. You used to pay 30% tax, and frank dividends based on 30% tax – that’s what produced the nice and clean no-double-tax scenario above. But because we now have a two-rate company tax system, the franking rules no longer work that way. There isn’t space here to explain how they now work, so cutting a long story short, when paying a dividend now out of that remainder 70% of profits, you could be required to frank it using the 26% tax rate. A smaller tax credit attaching to your dividend can only mean – you guessed it – a bigger top-up tax bill.

“You’re either managing your company’s franking outcomes or rolling the dice and taking your chances.”

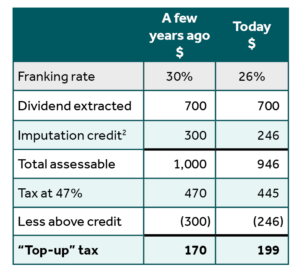

Example – how much top-up tax will you pay?

Here’s an example to illustrate. What is the ultimate tax borne on $1,000 of your company’s business profit from a few years ago? The company paid $300 in company tax at the time (ie, 30%), leaving $700, which you ultimately extract as a franked dividend, and let’s say you are on the top personal tax rate. Let’s see what the difference could be where you extracted that dividend a few years ago compared to extracting it today.

A few years ago, the $1,000 of profit ultimately bore tax at your personal rate of 47% (ie, the company paid $300, and you paid $170) – which is the whole point of the imputation system. But if you instead reinvested the 70-cents-in-the-dollar of after-company-tax profits into your business for a few years – very much necessary for most businesses – and only now extract it as a dividend, your top-up tax could now be $199.

Despite your personal tax rate of 47% – at which the imputation system is supposed to cap the total tax – the total tax borne on that $1,000 of business profit today would be just shy of 50% ($300 + $199 = $499). As predicted above, the double-tax arises in this example because your company today is permitted to attach a credit of only $246 out of the $300 tax paid a few years ago. You’re left with $501 today compared to $530 a few years ago.

It must be reiterated that the franking rate a company is now required to use when paying a dividend – 30% or 26% – is not automatically the same as its tax rate. The franking rate is now determined independently, and could be either one.

The opposite can be worse!

Of course, your situation could go the other way. Again cutting a long story short, your company might pay 26% tax now on your business’s profits, but when extracted as a dividend in future, could be required to frank using a 30% rate. That can result in the opposite outcome to above, where your company is forced to attach a tax credit to your dividend beyond the amount of tax your company has actually paid. That triggers a liability for Franking Deficit Tax, and if the deficit breaches certain tolerance limits, a 30% Franking Additional Tax penalty is imposed.

Actively manage

Sometimes, some of the above outcomes are unavoidable, but a lot of the time they can be mitigated by prudent management. But they must be managed by looking forward, not backwards. To be blunt, you’re either managing your company’s franking outcomes or rolling the dice and taking your chances.

Model outcomes, manage them

At Nexia Australia, we can model the above outcomes for your intended future extractions of profits from your business. If a double-tax impost would arise, the opportunity is there to determine if mitigating action can provide for a better outcome. It could mean hundreds of thousands of dollars staying in your pocket, or maybe much more.

Talk to your trusted Nexia Advisor about how we can assist with managing the tax outcomes from future extractions of your business’s profits.

1 It should be noted that if you are extracting your profits and spending it on private consumption, there is no magic wand that will get you out of bearing personal rates of tax.

2 A few years ago: $700 x 30/70 = $300. Today: $700 x 26/74 = $246