This publication replaces our November 2021 edition to incorporate the guidance issued by the ACNC for certain charities preparing special purpose financial reports to disclose Key Management Personnel remuneration and related party transactions, and the option to apply AASB 1060 disclosures.

At a glance

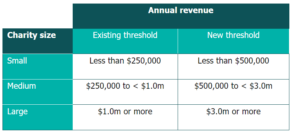

- The size thresholds which require charities to lodge audited or reviewed financial reports to the ACNC have been significantly increased from the 2021-22 financial year.

- For the 2021‑22 and subsequent financial years, large charities preparing special purpose financial reports will be required to include the Key Management Personnel (KMP) remuneration disclosures.

- For the 2022-23 and subsequent financial years, all medium and large charities preparing special purpose financial reports will be required to disclose other related party transactions in their annual financial statements.

- Charities preparing special purpose financial reports have a choice of applying either six mandatory standards or the AASB 1060 equivalent requirements.

The Australian Charities and Not-for-profits Commission Amendment (2021 Measures No. 3) Regulations 2021 has introduced the following important changes.

Reporting thresholds

In response to a recommendation in the ACNC Legislation Review, the financial reporting thresholds for charities registered with the ACNC have increased as follows:

The changes apply for the 2021-22 and subsequent financial years, ie, for 30 June 2022 balance dates. Based on the rules relating to substituted accounting periods (s60-85(2) of the ACNC Act), for 31 December balance dates the change will first apply to the 31 December 2022 financial year.

Related party disclosures for SPFRs

Medium and large charities preparing general purpose financial reports will apply either all accounting standards (Tier 1 GPFR) or AASB 1060 Simplified Disclosure Standard (Tier 2 GPFR). Both Tier 1 and Tier 2 general purpose financial reports include related party and key management personnel remuneration disclosures.

However, charities preparing special purpose financial reports (SPFR) under the ACNC Act only had to comply with five mandatory accounting standards – AASB 101, AASB 107, AASB 108, AASB 1048 and AASB 1054.

The new Regulation now prescribes AASB 124 Related Party Disclosures as an additional Australian Accounting Standard that must be applied by medium or large charities preparing SPFR. The Regulation also permits those charities a choice of applying either those six mandatory accounting standards or their equivalent paragraphs in AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For Profit and Not for Profit Tier 2 Entities (Simplified Disclosures Standard).

Where a charity chooses to apply the AASB 1060 option in its SPFR it should disclose that fact in the notes to the financial statements and make corresponding changes to its Responsible Persons’ declaration.

Remuneration disclosures for SPFRs

For the 2021‑22 financial year and subsequently, if a large charity has two or more key management personnel and prepares a special purpose financial report, it will be required to include disclosure of remuneration paid or payable to its KMP determined and measured in accordance with AASB 124. However, a Basic Religious Charity, regardless of size, does not have to report key management personnel remuneration in its SPFR.

The ACNC has provided relief so a large charity only needs to disclose total KMP remuneration without further dissection into separate categories of remuneration regardless of whether it chooses to apply the AASB 124 option or the AASB 1060 equivalent requirements. A charity can choose to voluntarily apply the full AASB 124 remuneration disclosures if it wants to.

Key management personnel of a charity may be employed by the charity or may be provided to the charity by a separate management entity or service company. Where key management personnel are not employed by the charity itself but provide services through a separate management entity, those amounts should be disclosed separately in the remuneration note.

The ACNC has also provided relief from including comparative KMP remuneration information in the first reporting year regardless of whether the charity applies the AASB 124 or AASB 1060 option. However, comparatives will be required in subsequent years.

There is no requirement for small or medium charities to make KMP remuneration disclosures in their special purpose financial report.

Disclosure of related party transactions in SPFRs

Where a medium or large charity prepares a special purpose financial report, the other related party disclosures contained in either AASB 124 or AASB 1060 will need to be included for the 2022-23 and subsequent financial years. For charities with a 31 December balance date, the change will first apply to the 31 December 2023 financial year.

There are no substantive differences between the other related party disclosures required by AASB 124 and AASB 1060.

A charity preparing SPFR and disclosing related party transactions for the first time in their 2023 annual financial report is not required to provide comparative information relating to the 2022 reporting period.

If you require assistance preparing for these changes, or for any further information, please contact your local Nexia Advisor.

Article by Martin Olde