The International Accounting Standards Board (“IASB”) has issued IFRS 16 Leases. The AASB and XRB will issue Australian and New Zealand equivalent standards, respectively.

The new standard will be effective for annual periods beginning on or after 1 January 2019. Early application is permitted, provided the new revenue standard IFRS 15 Revenue from Contracts with Customers is applied at the same date as IFRS 16.

Key impacts and implications

- For lessees, all leases other than short-term leases and low value leases will be recognised on balance sheet

- For lessors, there is little change to the existing accounting in AASB 117/IAS 17 Leases

- The profile of lease expense recognition changes

- Identification of lease and service components of arrangements becomes more important

- Changes to balance sheet and income statement will affect key ratios, banking covenants, remuneration and earn-out arrangements

- Effect on cash flow classifications in the Statement of Cash Flows

- Benefits of sale and lease back arrangements reduced

- Deferred tax consequences need to be considered

Lessee accounting

Initial recognition and measurement

Lessees are required to initially recognise a lease liability for the obligation to make lease payments and a right-of-use asset. The lease liability is measured at the present value of the lease payments to be made over the lease term.

The lease payments included in the measurement of the lease liability comprise the following payments during the lease term:

- fixed payments (including in-substance fixed payments), less any lease incentives receivable;

- variable lease payments that depend on an index or a rate, initially measured using the index or rate as at the commencement date;

- amounts expected to be payable by the lessee under residual value guarantees; the exercise price of a purchase option if the lessee is reasonably certain to exercise that option; and

- payments of penalties for terminating the lease, if the lease term reflects the lessee exercising an option to terminate the lease.

Importantly, a lessee isn’t required to estimate future variable lease payments linked to future performance or use of the asset, or a future index or rate (eg, CPI adjusted future lease payments). Rather, at each reporting period the lease liability and right-of-use lease asset is subsequently remeasured and adjusted for changes to future variable lease payments.

The right-of-use asset is initially measured at the amount of the lease liability plus the lessee’s initial direct costs (e.g., commissions) and an estimate of restoration, removal and dismantling costs.

Subsequent measurement

Lessees accrete the lease liability to reflect interest and reduce the liability to reflect lease payments made. The related right-of-use asset is depreciated in accordance with the depreciation requirements of AASB 116/IAS 16 Property, Plant and Equipment. For lessees that depreciate the right-of-use asset on a straight-line basis, the aggregate of interest expense on the lease liability and depreciation of the right-of-use asset generally results in higher total periodic expense in the earlier periods of a lease. Lessees remeasure the lease liability upon the occurrence of certain events (e.g., change in the lease term, change in variable rents based on an index or rate), which is generally recognised as an adjustment to the right-of-use asset.

Presentation

Right-of-use assets and lease liabilities are either presented separately from other assets and liabilities on the balance sheet or disclosed separately in the notes. Depreciation expense and interest expense cannot be combined in the income statement. Consequently, under IFRS 16 an entity’s EBIT and EBITDA will be different to that under existing standards as a result of the different measurement and presentation of expenses relating to leases. In the cash flow statement, principal payments on the lease liability are presented within financing activities; interest payments are presented in accordance with AASB 107/IAS 7 Statement of Cash Flows.

Key implications and effects

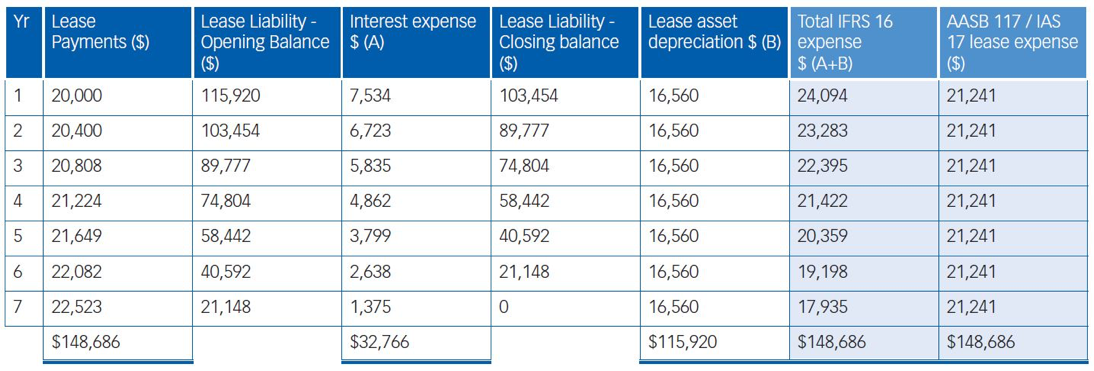

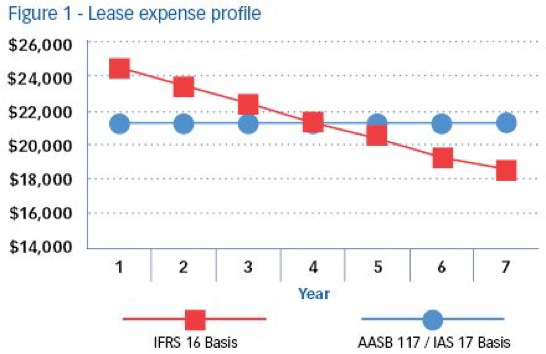

The following example illustrates the financial consequences of applying IFRS 16 and the comparison to the current lease standard.

Assume an entity enters into a non-cancellable 7 year equipment lease. There is no renewal option and the lessee’s initial direct costs are nil. Lease payments commence at $20,000 in year 1, increasing annually at 2%. The lessees’ incremental borrowing rate is 6.5%.

The initial measurement of the right-of-use asset and lease liability is $115,920. The lease asset is amortised on a straight-line basis over the lease term. Under AASB 117/IAS 17, the total lease expense is recognised on a straight-line basis over the lease term. Note that the total expense recognised in profit or loss over the lease term under IFRS 16 and AASB 117/IAS17 is the same. However, the pattern of the recognition of lease-related expenses differs, as illustrated below.

The expense recognition profile under IFRS 16 will affect certain financial ratios such as EDITDA, EBIT and Times Interest Cover. Changes to the balance sheet structure will also affect gearing ratios and Return on Capital Employed (ROCE).

The changes to lease accounting could affect some debt covenants. They could result in some entities no longer complying with debt covenants upon application of the new Standard if those covenants are linked to an entity’s IFRS financial statements. Entities should review their covenants to ascertain whether they are based on amounts determined in accordance with the accounting requirements in place at the time of signing the agreements, or in force at each measurement period.

IFRS 16 may also affect the regulatory capital of lessees that are AFS licensees or subject to other regulatory requirements.

The magnitude of the increase in operating profit, and finance costs, will depend on the significance of leasing to the lessee, the length of its leases and the discount rates applied. Although there may be accounting impacts on individual leases, lessees often hold a portfolio of leases, which could have the effect of neutralising any effect on profit or loss. For example, if a lessee’s lease portfolio is evenly distributed (ie the same number of leases start and end during a period and the lessee enters into new leases similar to those that end) the impact may be minimal.

A lessee classifies cash payments for: (a) the principal portion of lease liabilities within financing activities and (b) the interest portion of lease liabilities in accordance with the requirements relating to other interest paid, resulting in a general increase in cash flows from operating activities compared to existing requirements.

Operating leases and sale and lease-back arrangements have been common financing structures. However, as IFRS 16 requires lessees to recognise its lease liabilities, many current off balance sheet financial structures may become less appealing.

Lessor accounting

Initial recognition and measurement

The accounting by lessors under the new standard is substantially unchanged from current accounting in AASB 117/ IAS 17. Lessors classify all leases using the same classification principle as in AASB 117/IAS 17 and distinguish between two types of leases: operating and finance leases.

For operating leases, lessors continue to recognise the underlying asset. For finance leases, lessors derecognise the underlying asset and recognise a net investment in the lease similar to today’s requirements. Any selling profit or loss is recognised at lease commencement.

Subsequent measurement

For operating leases, lessors would generally recognise lease income on a straight-line basis. For finance leases, lessors recognise interest income for the accretion of the net investment in the lease and reduce that investment for payments received. The net investment in the lease is subject to the derecognition and impairment requirements in AASB 9/IFRS 9 Financial Instruments.

Short-term leases and leases of low value assets

The IASB has made accounting for short-term leases and low value leases easier. IFRS 16 permits lessees to make an accounting policy election, by class of underlying asset, to apply a method like AASB 117/IAS 17’s operating lease accounting and not recognise lease assets and lease liabilities for leases with a lease term of 12 months or less (i.e., short-term leases).

Lessees also are permitted to make an election, on a lease-by-lease basis, to apply a method similar to current operating lease accounting to leases for which the underlying asset is of low value (i.e., low-value assets). The assessment of whether an underlying asset is of low value is performed on an absolute basis. The assessment is based on the value of the underlying asset when it is new, regardless of the age of the asset being leased. Further, the assessment is not affected by the size, nature or circumstances of the lessee. Examples of low-value underlying assets can include tablet and personal computers, small items of office furniture and telephones. However, leases of cars would not qualify as leases of low-value assets because a new car would typically not be of low value.

IFRS 16 also permits a lessee to group individual leases with similar characteristics on a portfolio basis provided that doing so would not differ materially from applying the requirements to each individual lease.

Lease or service arrangement

IFRS 16 only applies to the accounting for a lease. A lease exists when the customer controls the use of an identified asset for a period of time in return for consideration. IFRS 16 requires that to control the use of an asset, a customer must have both exclusive use of the asset and direct the use of the asset.

A customer directs the use of an asset if it has the ability to change how and for what purpose the asset is used during the contractual term (for example, the ability to decide what the space in a leased retail unit is used for, or to decide where and when a leased ship sails). A customer also directs the use of an asset if it determines how the asset is operated or designed.

In some arrangements it may be unclear whether the customer controls the use of an identifiable asset (a precondition for a lease) or is obtaining a service which incorporates the utilisation of the supplier’s assets. The standard provides guidance on assessing whether an arrangement is a lease within the scope of IFRS 16, or a service arrangement.

Other arrangements may contain both a lease of an asset and associated services. A lessee separately accounts for lease components and service components within a contract.

To simplify the accounting for arrangements with multiple elements, IFRS 16 includes the option for a lessee to account for a lease component and related service components as a single lease arrangement instead of separating those components.

Lease term

Assessing the lease term is important as this forms the basis for calculating the value of the lease liability.

IFRS 16 defines the lease term as the non-cancellable period for which a lessee has the right to use an underlying asset, together with both:

- periods covered by an option to extend the lease if the lessee is reasonably certain to exercise that option; and

- periods covered by an option to terminate the lease if the lessee is reasonably certain not to exercise that option.

The lease term includes any rent-free periods provided to the lessee by the lessor.

A lessee needs to consider all relevant facts and circumstances that create an economic incentive for the lessee to exercise, or not to exercise, the option, including any expected changes in facts and circumstances from the commencement date until the exercise date of the option. These can include:

- contractual terms and conditions for the optional periods compared with market rates

- significant leasehold improvements incurred by the lessee

- costs relating to the termination of the lease, such as negotiation costs and relocation costs

- the importance of that underlying asset to the lessee’s operations.

Other requirements

The standard contains additional requirements and guidance relating to:

-

Identifying a lease, including:

- arrangements involving portions of assets;

- substitution rights;

- the right to direct the use of the underlying asset; and

- the effects of a lessor’s protective rights - Sub-lease arrangements

- Residual value guarantees and purchase options

- Lease modifications

- Sale and lease-back arrangements

Transition

The new standard permits lessees to use either a full retrospective or a modified retrospective approach on transition for leases existing at the date of transition, with options to use certain transition reliefs.

Next steps

IFRS 16 will be a significant change for lessees. Entities will need to closely review their lease arrangements and may need to form a number of judgements and estimates relating to lease terms; variable lease payments; low value assets; portfolio accounting and more.

Entities should perform a preliminary assessment as soon as possible to determine how their lease accounting will be affected. Entities will also need to consider:

- judgements required in assessing low value leases and portfolio groupings

- the impact on key metrics and ratios, debt covenants or remuneration arrangements

- any changes needed to processes (including internal controls) and systems to collect the necessary information.

For more information on IFRS 16 and how we can assist you implement these new requirements, please contact your local specialist.

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Australia. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Advisor. Liability limited by a scheme approved under Professional Standards Legislation other than for the acts or omission of financial services licensees.