Treasurer Jim Chalmers has delivered his second Budget, focusing on the goals of providing cost-of-living relief and managing inflation. These goals can come into conflict, and so a delicate balancing act is required.

The forecast deficit for the 2023-24 year is $13.9 billion, and the 2022-23 result, somewhat unexpectedly, is forecast to come in at a surplus of $4.2 billion (compared to the forecast $36.9 billion deficit in last October’s Budget). This will be the first surplus in 15 years. Whilst these numbers reflect a considerable improvement in the projected government’s finances, deficits will remain for the time being, and economic challenges persist, including high inflation, low productivity growth and low real wages growth.

The Government continues to invest in preventing serious financial crime, programs to promote GST compliance, and engaging with business in managing tax and superannuation liabilities. Business owners and investors will need to give attention to number of new measures.

We set out a summary of the key measures announced, and what they mean for you and your business.

Summary and highlights

We have set out a summary of the key measures announced, and what they mean for you.

See the following video for the highlights and read the complete summary below.

Alternatively, you can download a copy of the complete summmary here.

For further details in relation to these announcements, Nexia will also be hosting an online briefing on the 2023 Federal Budget on Thursday, 11 May 2023. Register here.

2023 Federal Budget Summary Contents

Contents: Scroll to Individuals / Scroll to Businesses / Scroll to Superannuation / Scroll to International / Scroll to Other

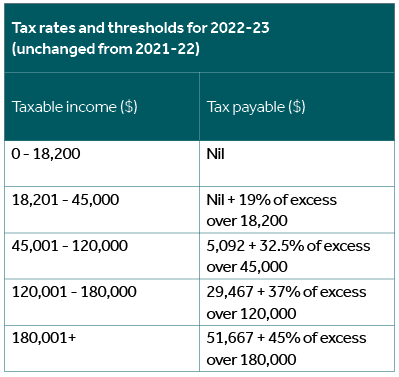

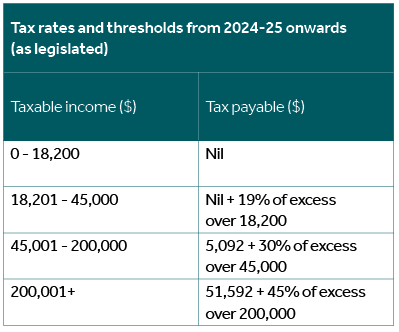

1. No change to personal tax rates

The Government has again left the previously legislated personal tax rate changes unchanged.

With no announcement of any changes to the personal tax rates, the Stage 3 tax changes will commence from 1 July 2024, as legislated. Under the Stage 3 tax changes, the 32.5% marginal tax rate will be reduced to 30% for the income bracket between $45,000 and $200,000. The 37% tax bracket will be completely removed from the 2024-25 income year.

This means that the following individual income tax rates will apply (excludes the 2% Medicare levy):

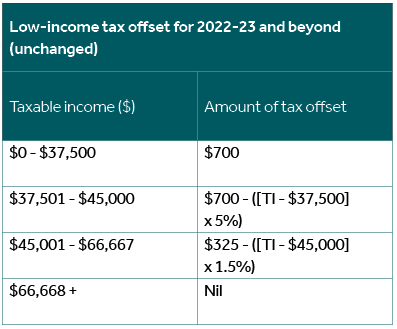

2. Low-and-middle-income tax offset not extended

Originally introduced in the 2019 Budget, the low-and-middle-income tax offset (LMITO) was previously extended to the 2021-22 income year as a temporary tax relief measure for individuals whose taxable income was below $126,000. For the year ended 30 June 2022, eligible individuals were entitled to a non-refundable tax offset of up to $1,500 ($3,000 for couples) upon lodgement of their individual income tax returns.

No further extension of the LMITO was announced in this Budget. As such, the LMITO has now ceased (with the 2021-22 income year being the final year), and now replaced by the low-income tax offset.

3. Cost-of-living relief

The government has announced a $14.6 billion package aimed at tackling the rising cost of living over the next four years. With last October's Budget forecasting a 56 per cent increase to electricity bills over the next 18 months, $1.5 billion has been dedicated to electricity bill relief for more than 5 million households and a further 1 million small businesses. Eligible beneficiaries, including pensioners, small businesses, and individuals receiving income support, will have their bills subsidized by up to $500. The extent of the support is dependent on which state or territory the recipient lives in.

Contents: Individuals / Businesses / Superannuation / International / Other

1. Instant Asset Write-Off Threshold of $20,000 for Small Business

Small businesses (group-wide turnover less than $10 million) currently benefit from an unlimited instant asset write-off which is due to end on 30 June 2023. The Government will temporarily retain an instant asset write-off for the full cost of eligible assets costing less than $20,000 (excluding any GST credit) that are first used or installed for use between 1 July 2023 and 30 June 2024. The threshold of $20,000 will apply on a per-asset basis. Effectively, small businesses will be able to claim a tax deduction for the full cost of multiple assets.

Assets costing $20,000 or more (which cannot be immediately deducted) can continue to be placed into the small business simplified depreciation pool and depreciated at 15% in the first income year and 30% each income year thereafter.

2. Small business energy incentive

Businesses with an annual turnover of less than $50 million will receive an additional 20% deduction on investments that support energy-efficient practices and implementing energy-saving technologies. The purpose is to encourage making investments like electrifying heating and cooling systems, upgrading to more efficient fridges and induction cooktops, and installing batteries and heat pumps.

The measure is part of a larger push to ensure that small business operators can share in the energy transition that is now underway, whilst also helping Australia lower its emissions.

Up to $100,000 of total expenditure will be eligible, allowing a maximum bonus tax deduction of $20,000 per business.

Eligible assets or upgrades will need to be installed and ready for use between 1 July 2023 and 30 June 2024 to qualify for the bonus 20% deduction.

3. Petroleum Resource Rent Tax and Mining, Quarrying and Prospecting Rights

The petroleum resource rent tax (PRRT) applies to offshore petroleum projects. The PRRT is the equivalent to State government mining royalties but as the extraction takes place offshore, the Commonwealth rather than the States have jurisdiction.

Petroleum projects require extremely high upfront capital investment and generally many years will be required before the project starts to generate income. Both capital and revenue expenditure are “uplifted” - like being indexed but generally at substantially better rates to reflect project investment risk – and the uplifted amounts are carried forward and are deductible for petroleum resource rent tax purposes. The quantum of the required capital expenditure together with the effect of uplifting means that, under current law, petroleum resource rent tax will not start to be payable in respect of a project until many years after the project has started to generate income. Under the current rules, most LNG projects are not expected to pay significant amounts of PRRT until the 2030s.

From 1 July 2023 or seven years after the date of first production, whichever is the later, the Government will limit the proportion of PRRT assessable income of LNG projects that can be offset by most deductions to 90 per cent. That is, 10% of PRRT income from LNG projects will not be able to be reduced by most deductions. This means that some petroleum resource rent tax at least should generally be payable within seven years of an LNG project’s date of first production.

The Government will specifically narrow the definition of “exploration” in the PRRT legislation to ensure that exploration does not extend to the evaluation of whether the resource is commercially recoverable. The Government will also clarify that mining, quarrying and prospecting rights cannot be deducted for income tax purposes until they are used (not merely held) and will limit the circumstances in which the issue of new rights over areas covered by existing rights give rise to tax adjustments.

The Government will also proceed with the implementation of a range of technical and integrity measures in relation to PRRT recommended by the Treasury Gas Transfer Pricing Review and the Callaghan Review.

4. No new tax concessionary regime for income from patents

The previous Government had announced that a concessionary “patent box” regime would be introduced under which income from certain kinds of patents would be taxed at a lower rate. The current Government has announced that they will not be proceeding with this measure.

5. Reduction of Statutory GDP Adjustment Factor for PAYG and GST Instalments

The ATO calculates PAYG and GST Instalments using information from the previous year’s tax return which is indexed using a GDP Adjustment Factor to account for any likely growth in income from the prior year.

The statutory GDP Adjustment Factor has been reduced to 6% for the 2023-24 income year, halving the 12% which would have applied under the statutory formula.

The reduced GDP uplift rate of 6% will provide cash flow support for small businesses eligible to use the relevant instalment methods (up to $10 million group-wide turnover for GST Instalments and $50 million group-wide turnover for PAYG instalments). This factor has been reduced to provide cashflow support throughout the pandemic from the 2020-21 to 2022-23 income years. As Australia’s economy recovers from pandemic conditions, the indexation will trend closer to the statutory formula.

6. Driving collaboration with small business

The Budget has focused on reducing paperwork for small businesses. Accountants and tax agents will be able to lodge multiple Single Touch Payroll forms on their clients’ behalf from 1 July 2024, lessoning the burden on the employer to lodge the forms monthly. From 1 July 2024, small business will also benefit from faster and safer tax refunds by reducing the use of cheques.

From 1 July 2025, small businesses will be granted up to four years to amend their income tax returns, “reducing the burden of making revisions”.

It was also announced in the Budget to lower the tax-related administrative burden on small business that from 1 July 2025 there will be $9 million provided over 4 years on tax clinics to improve access to tax advice. There will also be $12.8 million over 3 years commencing from 1 July 2024, to trial an expansion of the ATO independent review process to small businesses that are being subjected to an ATO audit. This trial is proposed to run for 18 months.

7. Lodgment penalty amnesty for small businesses

In an effort to encourage small businesses with outstanding tax statements to re-engage with the ATO, the Government has announced that it will provide a temporary lodgment penalty amnesty to small businesses with group-wide turnover of less than $10 million. The amnesty will remit failure-to-lodge penalties for outstanding tax statements lodged in the period from 1 June 2023 to 31 December 2023 that were originally due during the period from 1 December 2019 to 29 February 2022.

Contents: Individuals / Businesses / Superannuation / International / Other

1. Employer Payday Super Obligations

From 1 July 2026, employers will be required to pay an employee’s superannuation at the time that they pay their wages. This change will affect all employers, but the Government has provided a three-year lead-in period in order to allow employers adequate time to adjust their systems accordingly.

Employees’ superannuation was always part of their remuneration, but in the past this change would have imposed a significant administrative burden on employers. The efficiencies of modern-day computerised and automated payroll functionality that virtually all employers have, especially through the compulsory adoption of Single Touch Payroll, now makes this change feasible. However, employers will need to appropriately manage their cashflow, as this change will bring forward employee superannuation payments.

2. Additional Resourcing to Enforce Superannuation Compliance

The Government is providing more resourcing to the ATO to enable them to detect unpaid employer superannuation obligations earlier. In addition, the ATO will be set enhanced targets for the recovery of all such unpaid superannuation for employees. The underlying message here is that employers who are not up to date with their employee superannuation obligations face a heightened risk of detection, which comes with significant penalties.

3. Additional tax on higher super account balance

From 1 July 2025, an additional 15% tax on the “earnings” will apply to individuals with a Total Superannuation Balance (TSB) of more than $3 million on any subsequent 30 June.

Earnings for this purpose will be calculated using a formula, reflecting the change in the value of the TSB at the start and end of the financial year, excluding the effect of withdrawals and contributions. This means that any unrealised gains and losses will be included in the calculation. The $3 million threshold applies to individuals of all ages, even if an individual is not eligible to access their superannuation benefits.

The additional tax will be assessed to the individual, who can pay it personally, or choose for the tax to be paid from their superannuation fund.

Individuals with a TSB balance of less than $3 million at 30 June in a year will not be affected.

4. Non-arm’s length income

From 1 July 2023, an effective tax rate of 90% will apply to self-managed superannuation funds (SMSFs) or a small APRA-regulated funds (with 6 or fewer members) in relation to certain expenses. Under the non-arm's length income (NALI) provisions, if the fund incurs a general expense that is not at arm’s length terms, the punitive tax impost applies to the taxable income equivalent to the shortfall amount.

Contents: Individuals / Businesses / Industry / Superannuation / International / Other

1. Expanding the general anti-avoidance regime

The Government will expand the scope of the general anti-avoidance regime of Part IVA so that it applies to:

- schemes that reduce tax paid in Australia by accessing merely a lower (as opposed to nil) withholding tax rate on income paid to foreign residents; and

- schemes that achieve an Australian income tax benefit, even where the dominant purpose was to reduce foreign income tax.

This measure will apply to income years commencing on or after 1 July 2024, regardless of whether the scheme was entered into before that date.

Contents: Individuals / Businesses / Superannuation / International / Other

1. Boost to invest in build-to-rent accommodation

The Government will offer two tax incentives for investors to increase the supply of rental housing by changing arrangements for investments in built-to-rent accommodation:

- Increase the depreciation rate from 2.5 per cent to 4 per cent per year for eligible new build-to-rent projects where construction commences after 9 May 2023.

- Reduce the withholding tax rate for eligible fund payments from managed investment trusts to foreign residents on income from newly constructed residential build-to-rent properties after 1 July 2024 from 30 to 15 per cent, subject to further consultation on eligibility criteria.

Contents: Individuals / Businesses / Superannuation / International / Other

Final word

Following last October’s “bread and butter” Budget of modest policy announcements, this year’s Budget reflects improving, but mixed, government finances, with further “modest but meaningful” reform measures.

It has been extensively documented that persistent low productivity growth is a key reason why low unemployment has not translated into real wages growth. A more ambitious reform agenda is needed to improve productivity, removing constraints on businesses and individuals meeting today’s challenges and preparing for future ones.

Talk to your trusted Nexia advisor about what any of the Budget announcements mean for you or your business.