Monthly Highlights

Global share markets rebounded strongly in April, with some major markets reaching record highs, as investors looked through ongoing Middle East tensions and focused on a reduced risk of broader escalation. The ceasefire helped stabilise sentiment, though oil prices remained elevated amid ongoing energy supply disruptions. Renewed enthusiasm for AI and stronger-than-expected US corporate earnings also supported the recovery in shares, while bond markets remained cautious amid persistent inflation and interest rate concerns.

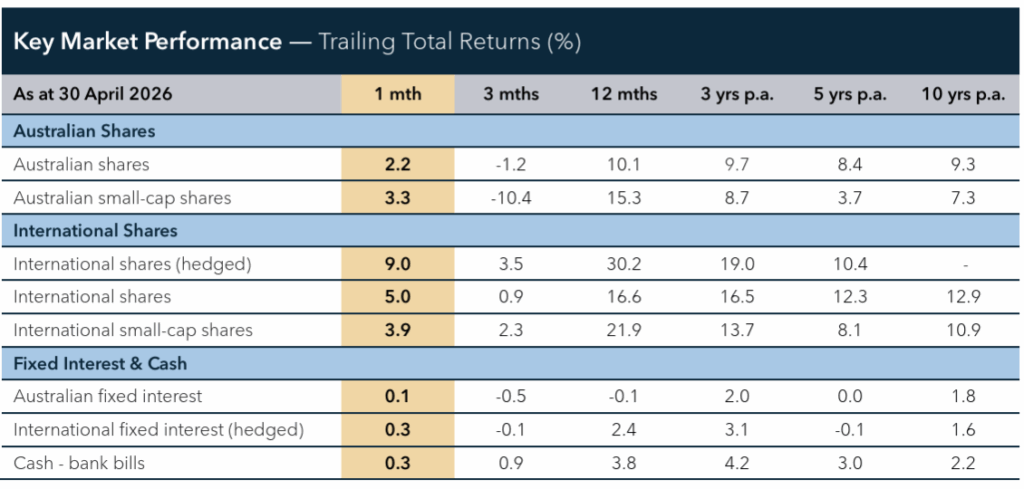

Australian shares delivered positive returns but lagged major global markets. Gains were led by information technology, materials and property, while more defensive sectors such as healthcare and consumer staples underperformed. Energy also declined, reflecting some profit-taking after the prior month’s strong rise. The domestic interest rate backdrop remained a key focus, with the RBA’s consecutive rate rises in February, March and May effectively reversing last year’s rate cuts.

International shares rose strongly across developed and emerging markets. The US delivered an exceptional rebound, supported by technology and growth companies, while Europe and Japan also posted strong gains. Emerging markets were particularly strong, helped by renewed enthusiasm for companies linked to the AI supply chain, particularly in Korea and Taiwan. For Australian investors, a stronger Australian dollar acted as a headwind to unhedged global share returns.

Australian and global fixed interest markets stabilised following March’s sell-off and posted modest gains in April. Government bond yields remained elevated as investors focused on inflation and the prospect of tighter policy settings. Credit markets strengthened, with high yield credit outperforming as investor confidence improved.

Market Observations

The global investment backdrop has become more complicated following escalating tensions in the Middle East and disruptions to energy supply. Rising oil and gas prices are flowing through to transport, manufacturing and household costs, increasing uncertainty around inflation, interest rates and economic growth. Despite these challenges, global share markets rebounded strongly through April, supported by resilient earnings and renewed enthusiasm around AI and technology stocks.

While markets have remained resilient so far, investors are increasingly focused on whether higher energy costs begin to place greater pressure on growth and inflation. Importantly, current conditions still point to slower growth rather than a severe global recession, with the global economy continuing to benefit from relatively healthy corporate and consumer balance sheets. The global economy is also less sensitive to oil shocks than in previous decades due to greater energy efficiency and a more diversified energy mix. However, prolonged disruption would still place meaningful pressure on growth, particularly in countries heavily reliant on imported energy.

Against this backdrop, inflation has again become the key focus for central banks and investors alike. Central banks are increasingly reluctant to overlook higher energy prices after the inflation challenges of recent years. While inflation expectations remain relatively contained, rising input costs and relatively tight labour markets have increased the risk that interest rates remain elevated for an extended period. This has contributed to rising bond yields and greater market volatility, although broader investor sentiment has remained resilient.

These pressures are affecting economies differently. The US economy continues to show resilience, supported by healthy consumer activity, strong labour markets and ongoing investment in structural growth areas such as AI. Australia, however, appears more vulnerable. Inflation remains elevated, household pressure is intense and higher energy costs are adding to the strain on an already slowing economy. With inflation proving more persistent than hoped, the RBA has raised rates in three successive meetings, back to the post-pandemic peak of 4.35%, citing rising fuel costs and signs businesses are passing higher costs on to consumers.