What is new and important for FBT 2026?

- Plug-in hybrid electric vehicles (PHEVs) are no longer treated as zero or low emissions vehicles for FBT purposes from 1 April 2025, unless transitional rules apply.

- Eligible battery electric, hydrogen fuel cell and similar zero or low emissions cars can still access the electric car exemption where the eligibility conditions are met.

- The ATO’s alternative record-keeping concession continues for eligible benefits, allowing employers to use existing business records instead of prescribed declarations or travel diaries in some cases.

- Car parking remains an ATO focus area. For the FBT year ending 31 March 2026, the car parking threshold is $11.03 per day.

- Employers should also review entertainment, exempt work-related items, living-away-from-home arrangements, employee loans and motor vehicle logbooks before lodgment.

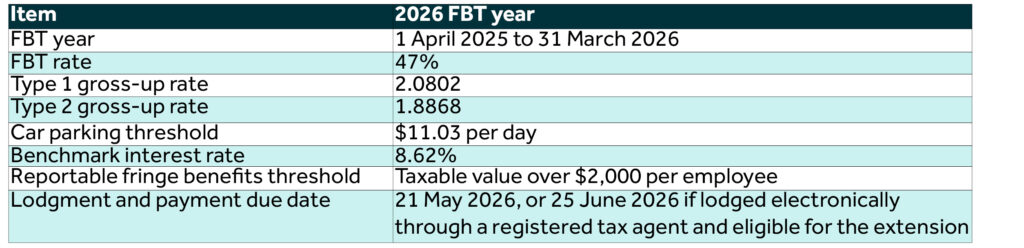

2026 key FBT rates and thresholds

Vehicle benefits: what should businesses check now?

Vehicle benefits: what should businesses check now?

- Review all employer-provided vehicles, including company cars, novated leases and salary packaged vehicles.

- If a PHEV arrangement was first entered into on or after 1 April 2025, the electric car exemption generally no longer applies.

- For exempt electric cars, employers still need sufficient records to support eligibility, including when the car was first held and whether the car was below the relevant luxury car tax threshold at first retail sale.

- Where the operating cost method is used, confirm odometer records and logbooks are current and valid.

- Do not assume that utes, dual cabs, vans or other commercial vehicles are automatically exempt. Private use still needs to be tested carefully.

Common FBT issues

- Director and shareholder benefits in private companies being treated informally without FBT review.

- Entertainment expenses posted to general ledger accounts without being classified correctly for FBT, income tax and GST purposes.

- Car parking not being reviewed where staff park near commercial parking stations.

- Missing employee declarations, outdated logbooks or incomplete support for otherwise deductible claims.

- Staff reimbursements and credit card payments being treated as deductible business costs without considering whether an expense payment fringe benefit arose.

Year-end action plan for employers

- Identify all non-cash benefits provided to employees and associates during the period 1 April 2025 to 31 March 2026.

- Review motor vehicles, entertainment, employee reimbursements, loans, housing, meal benefits and work-related items.

- Confirm which benefits are exempt, which are reportable, and which require gross-up for FBT calculation purposes.

- Gather supporting records early, including logbooks, invoices, declarations, lease documents and payroll data.

- Confirm reportable fringe benefits amounts are correctly included in STP finalisation by 14 July 2026 where applicable.

How we can help

Nexia can assist with year-end FBT reviews, calculation of taxable benefits, classification of entertainment expenses, vehicle benefit analysis, electric vehicle exemption reviews, and preparation and lodgment of your 2026 FBT return.