What has happened

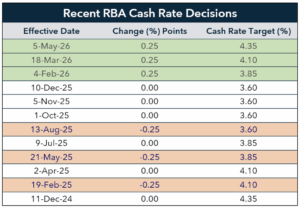

The Reserve Bank of Australia (RBA) today increased the cash rate by 25bp to 4.35%. The move was widely anticipated, with money markets having ascribed approximately a 70% probability to a rate rise today and the clear majority of economic forecasters expecting the same.

Having cut rates three times across 2025, the RBA has now hiked rates three times in succession, in February, March and now in May 2026. The 75bp of easing delivered last year has been entirely reversed, with the cash rate back at its post-pandemic peak of 4.35%.

Eight of the nine Board members voted to increase the cash rate today, while one member voted to leave policy unchanged. This differs from the March Board meeting, when five members voted to raise rates and four voted to keep policy on hold. As such, the Board as a collective has today shifted in a hawkish direction.

At 4.35%, monetary policy is now in restrictive territory, meaning the RBA is deliberately applying the brake to slow the economy. Even if the war in Iran were resolved tomorrow, the effect of higher borrowing costs would slow economic growth and modestly push unemployment higher over the course of 2026. This is intentional. Inflation remains too high, and the central bank’s job is to bring it down by cooling demand across the economy.

The ongoing conflict in the Middle East has added a significant layer of uncertainty to the outlook. Notwithstanding, the RBA judged that the policy choice of least regret was to raise rates again, largely because domestic price pressures were already running too hot before the conflict began. The war has simply added to these price pressures.

On that score, the Statement accompanying the Board decision noted that higher fuel prices from the war in the Middle East are “likely to have second-round effects on prices for goods and services more broadly. This inflation impulse is in addition to the high inflation recorded around the start of 2026, reflecting capacity pressures in the economy”.

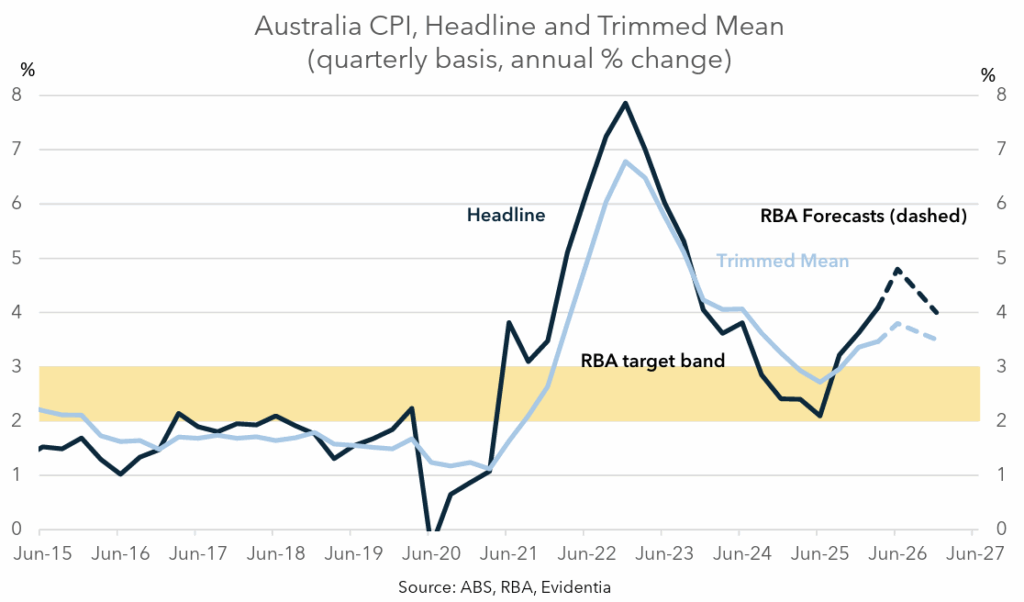

Inflation: the numbers behind the decision

The RBA has made a material upward revision to its inflation forecasts in its May Statement. The central bank now expects headline CPI, the broadest measure of inflation, to peak at 4.8%/yr in Q2 26, before gradually declining. The trimmed-mean, which strips out the most volatile price movements and is the RBA’s preferred measure of inflation, is forecast at 3.8% per year over the same period.

The gap between headline and trimmed mean inflation largely reflects higher fuel prices driven by the war in Iran. Headline inflation is the figure that feeds into wage negotiations, rent reviews and government benefit adjustments each year — and it is the measure that most directly shapes how households feel about the cost of living. The RBA monitors both, but the consequences of elevated headline inflation extend well beyond what the trimmed mean alone captures.