The ongoing conflict involving Iran, the US and Israel has added a new source of uncertainty to global financial markets. Events in the Middle East are always closely watched by investors, given the region’s importance to global energy supply, and the current conflict has already begun to affect investor sentiment.

At present, the Strait of Hormuz supply channel is effectively closed. This narrow shipping route is one of the world’s most important energy corridors, and disruption to traffic through the Strait has pushed oil prices sharply higher.

Periods like this can understandably create anxiety for investors. Market moves can be rapid, and headlines can shift quickly as events unfold. While the seriousness of the situation should not be understated, it is also important to keep some perspective. Financial markets have navigated many geopolitical shocks in the past, and the initial phase of volatility rarely tells the full story of how markets ultimately respond.

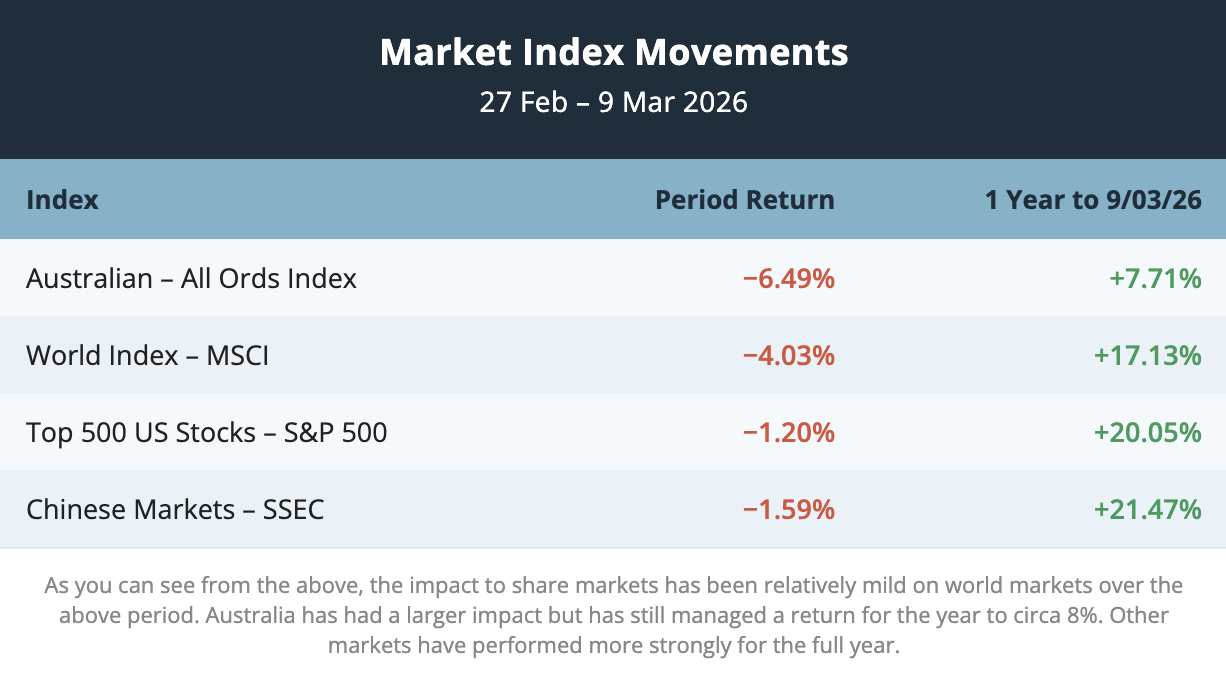

Market index movements

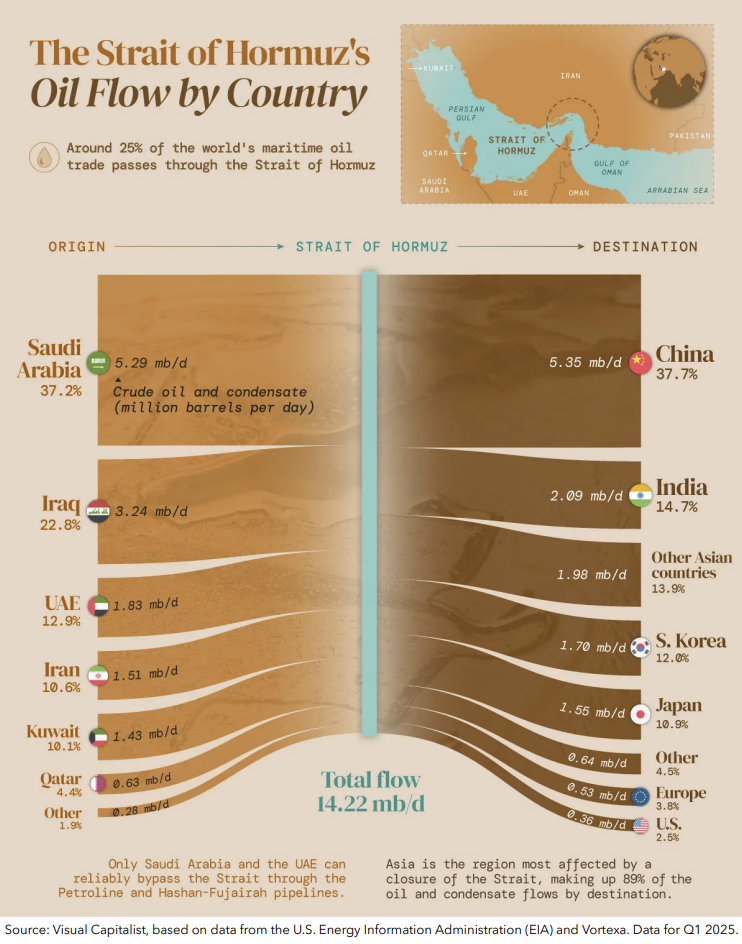

Why the Strait of Hormuz matters

The Strait of Hormuz is one of the world’s most important shipping corridors. A significant share of global oil exports moves through this narrow waterway each day, making it a critical route for energy supply. With shipping traffic through the Strait now effectively halted, markets have quickly priced in the risk of supply disruption.

Because energy sits at the centre of the global economy, movements in oil prices tend to transmit rapidly into financial markets. Higher energy costs can ripple through the broader economy, affecting transportation, manufacturing, and consumer spending.

The graphic below highlights how dependent global energy trade is on the Strait of Hormuz. A large share of oil exported from Saudi Arabia, Iraq, the UAE and other Gulf producers passes through this route before reaching international markets.

Importantly, most of these flows are destined for Asia. Countries such as China, India, Japan and South Korea rely heavily on oil shipments that pass through the Strait, making their economies particularly sensitive to disruptions in the region. By contrast, the US is far less exposed due to its domestic energy production.

What this could mean for inflation and the economy

Energy prices are one of the main channels through which geopolitical events affect the global economy.

If oil prices remain elevated for a sustained period, higher fuel costs can feed through to transportation, manufacturing and food prices. This dynamic was evident following Russia’s invasion of Ukraine in 2022, when energy and agricultural supply disruptions pushed inflation higher around the world. Earlier episodes in the 1970s showed similar patterns, with prolonged oil supply disruptions contributing to higher inflation and weaker economic growth.

The risk is also broader than oil alone. The Strait of Hormuz is a critical route not just for crude exports, but also for liquefied natural gas, with about one-fifth of global LNG trade passing through the Strait, largely from Qatar. Natural gas is a key input in nitrogen fertiliser production, which means a prolonged disruption could also place upward pressure on fertiliser and, over time, food costs.

The ultimate economic impact will depend largely on how long energy prices remain elevated.

Market reaction so far

Global markets initially reacted in a relatively measured way to the early stages of the conflict. However, as oil prices rose and the disruption to shipping became clearer, selling pressure intensified across Australia, Asia and Europe.

Overnight, sentiment improved. US markets recovered from early losses, volatility eased, and Australian share futures pointed to a sharp rebound at the open. The improvement appeared to reflect several factors, including oil pulling back from its intraday highs, comments from President Trump suggesting the conflict may end sooner than feared, and indications that G7 countries stand ready to support global energy supply if required.

This remains an oil-led market. Brent crude briefly surged toward US$120 a barrel as traders priced in the risk of a prolonged supply shock. Prices have since fallen sharply and are now trading just below US$90 a barrel as immediate fears of a sustained disruption have eased.

Bond markets have also responded. Higher oil prices raise the risk that inflation may prove more persistent than expected, complicating the outlook for interest rates. As a result, government bond yields have risen as markets reassess the path of central bank interest rate decisions.

During episodes like this, markets often become focused on a single dominant variable. At present, that variable is oil prices.

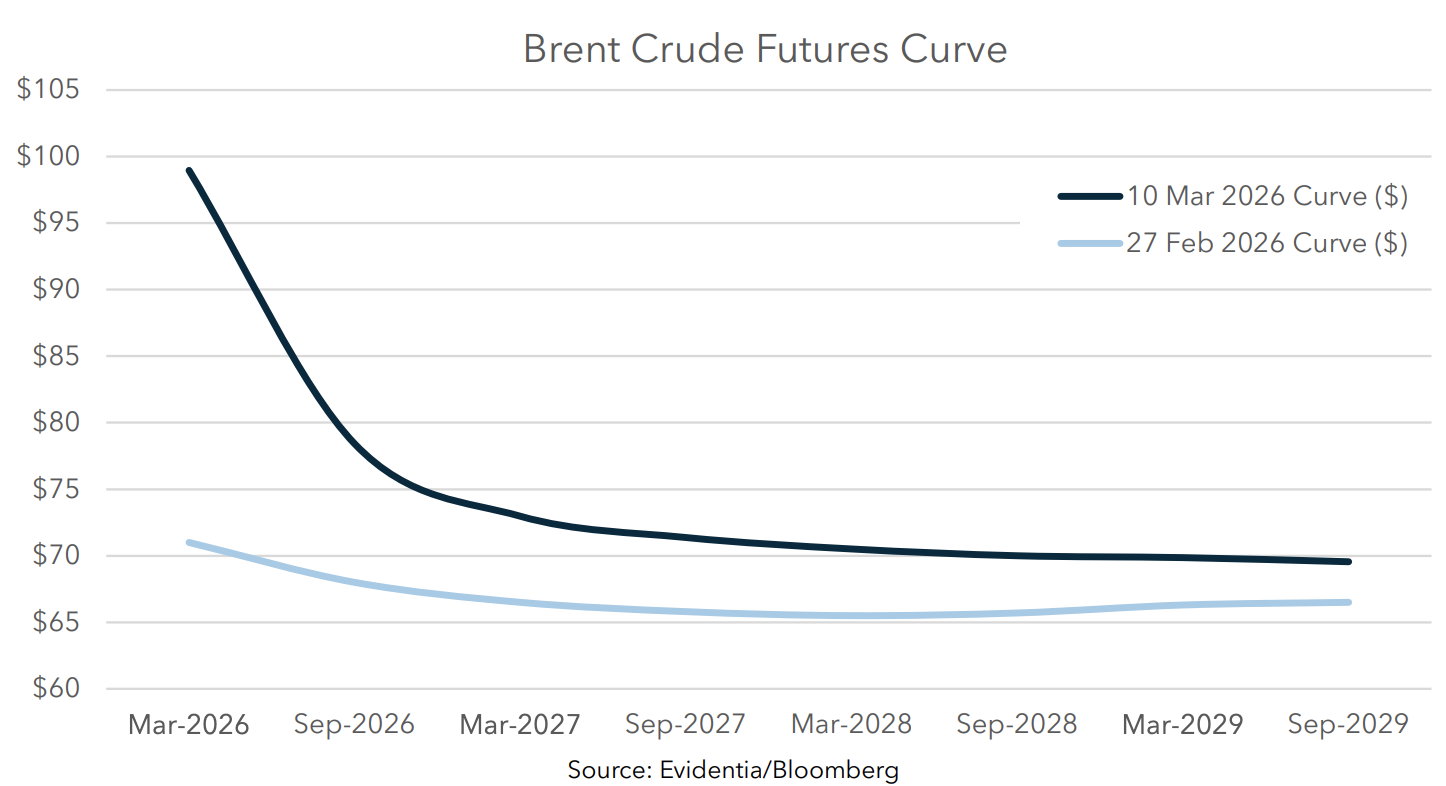

What the oil market is signalling

For markets, the key question is not simply how high oil prices rise, but how long they remain elevated.

Near-term oil prices initially spiked as traders priced in immediate supply risks. However, prices further out along the futures curve — which shows the price the market expects oil to trade at in the months and years ahead — remain noticeably lower. This suggests markets currently expect supply conditions to stabilise once tensions ease.

The chart below compares the oil futures curve before the conflict escalated with today’s curve. Near-term prices have jumped sharply, but prices further out remain similar, suggesting markets still expect the shock to be temporary.

This distinction is important. The economic impact of an oil shock depends heavily on its duration. A temporary spike in energy prices can usually be absorbed by the global economy. A prolonged period of elevated oil prices would be more problematic, placing pressure on inflation, company earnings and household spending.

Possible paths from here

Given the uncertainty surrounding the conflict, it is helpful to think about a range of potential outcomes.

One possibility is that tensions remain elevated but contained. In this scenario, oil prices remain volatile, but energy supply ultimately continues to flow, limiting the broader economic impact.

A second scenario would involve further escalation, keeping oil prices elevated for longer. This would increase inflation pressures and weigh more heavily on global economic growth.

The most severe outcome would involve a sustained disruption to shipping through the Strait of Hormuz. This remains a lower-probability outcome, but would represent a more significant supply shock to the global energy system.

At present, markets appear to be pricing conditions somewhere between the first two scenarios, with the most extreme outcome still considered a tail risk.

What history tells us

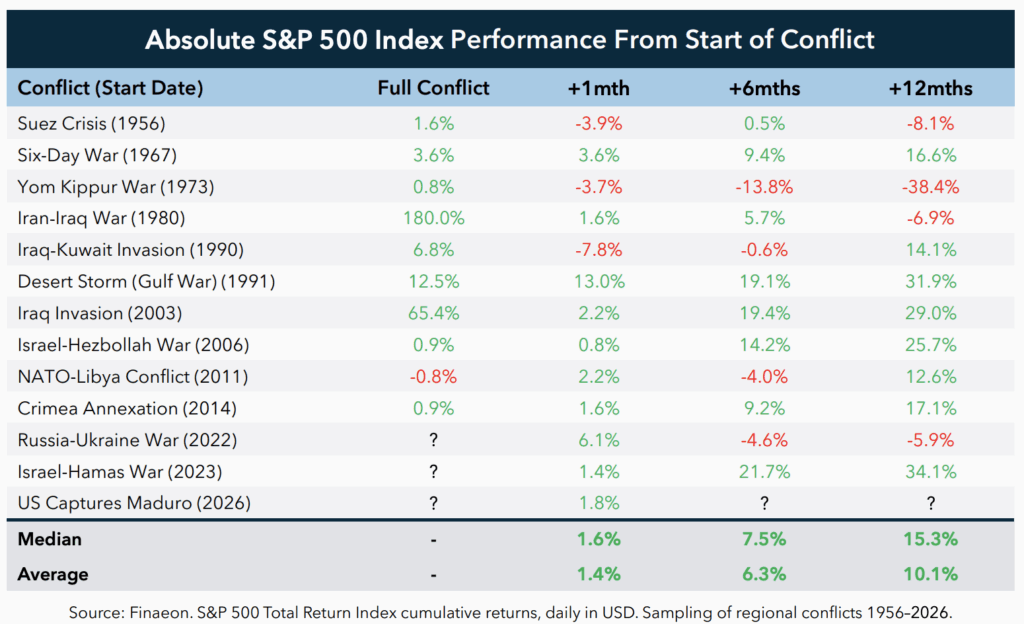

Geopolitical events often trigger sharp short-term market reactions. However, history shows that markets recover relatively quickly from geopolitical shocks.

The table below highlights how the US share market has performed following the outbreak of several major geopolitical conflicts over the past seventy years. While markets often experience volatility in the weeks immediately following these events, the majority of episodes have been followed by positive returns over the subsequent six to twelve months.

This pattern reflects the forward-looking nature of financial markets. Once investors become confident that an event will not permanently impair global economic activity, attention typically returns to the underlying drivers of markets such as earnings growth, interest rates and liquidity.

For long-term investors, this historical perspective is important. Short-term volatility during geopolitical crises is common, but it has rarely altered the long-term trajectory of markets.

What this means for portfolios

Periods of uncertainty are an unavoidable part of long-term investing. Our focus remains on the fundamentals of the assets held within portfolios and how evolving conditions may affect them. We continue to monitor developments closely, particularly the path of oil prices, inflation expectations and global economic conditions.

At this stage, remaining invested remains the most sensible course of action, as market rebounds often occur quickly once uncertainty begins to ease.

If the current disruption proves temporary, markets could recover just as quickly as they have fallen. If the situation evolves into a more prolonged supply shock and markets move lower from here, periods of volatility may also create attractive opportunities to invest in high-quality assets at more compelling valuations.

Maintaining discipline during periods of market stress has historically been far more effective than reacting to short-term headlines. Well-diversified portfolios are designed with exactly these kinds of periods in mind.

Next steps

We’re here to support you through all market conditions. If you have any questions or would like to discuss anything about your portfolio in more detail, please don’t hesitate to reach out.