A dark turn

We recently wrote about a new tax law applying from 1 July under which a business will be denied a deduction for gross wages and other payments if it fails to withhold, or withholds but fails to report to the ATO. The simple solution to ensure your deduction is not denied is to withhold when required, lodge your BASs/IASs on time, and keep your Single Touch Payroll reporting up to date. It’s another matter entirely if you don’t have the money to pay, reflecting a bigger concern, being cashflow difficulties.

But as often happens, Part 2 is when the story takes a dark turn. Which brings us to that age-old matter for many businesses of correctly classifying the people you’re paying as employees or contractors. Your obligations are very different between the two, and the classic risk scenario is paying people on the basis they are contractors, for the ATO to then conduct a review and take the view that they are in fact employees.

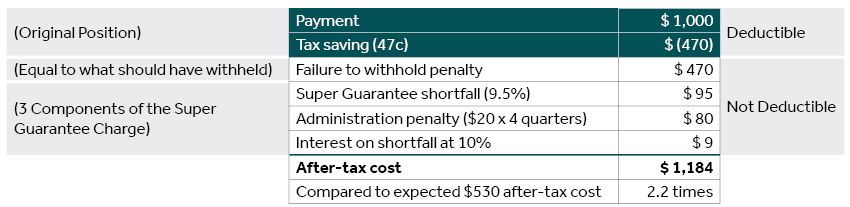

Let’s stop for a moment, and consider the consequences of this under the law as it will stand for only a few more days. Let’s say you paid $1,000 (ex-GST) a year ago to someone you regarded as a contractor (who quoted their ABN on their invoice). Using the top personal tax rate of 47 cents, your after-tax cost is $530 (ie, $1,000, less 47% tax saving). Imagine the ATO now conducts a review, and takes the view that the person was in fact your employee. The outcome might look like this:

Mistakenly treating someone as a contractor could more than double what you thought the after-tax cost to your business would be. If that wasn’t bad enough already, the consequences of such a mistake are about to get much worse. Currently, the $1,000 paid to your contractor – no, wait; employee, according to the ATO – is still deductible. However, from 1 July, the new law applies. As you didn’t withhold from a payment to an employee (let alone report it), the payment is not an allowable deduction. So, the after-tax cost to your business now becomes this:

Getting the employee vs contractor question wrong was already a costly mistake; now it could be devastating. A dark turn indeed.

Or is it?

But here’s the more interesting part – the Explanatory Memorandum (EM) accompanying the Bill enacting this new law contains a subtle hint of a gap between what the law requires of you, and what the Government nonetheless expects of you. There is an exception to this new rule denying your deduction where the person you paid gave you an invoice that quotes their ABN. That’s it. The law requires nothing further for this exception to apply.

So, shouldn’t this exception apply in the above example? The contractor/employee provided an invoice and ABN, and thus the $1,000 remains deductible, right?

Well, according to the EM, no, that’s not enough.

The EM states that the Government recognises that the deduction should not be denied where an employer “honestly believes their employees are acting as contractors.” Further, the EM contains an example where an employer, believing they were engaging contractors, is not denied a deduction for the payments due to their failure to withhold. The key sliver of information in the example is that the employer had earlier sought professional advice, which concluded that their people were contractors. Whilst the ATO disagreed with the advice, the point is that the employer at least sought external verification.

The subtle message is that, for the exception to apply, receiving an invoice with an ABN from your contractor/employee is not enough – despite the law requiring nothing more. Rather, the Government wants to see that an employer has done something beyond the demands of the law itself. You can argue all you like with the enforcers of this law – the ATO – that you have met the requirements of this exception. However, it’s very easy for the ATO audit team to simply deny the deduction and issue an amended assessment. Job done. If you want to object, well, you have to take that up with a different department in the ATO.

The ATO is increasingly reviewing employee/contractor arrangements, aided by the Taxable Payments Annual Report (TPAR) obligations for businesses in industries like construction, couriers, cleaning, transport and IT.

So, yes, it is a dark turn

The moral of the story is that if there is the slightest pause upon asking the question of whether any of your people are employees or contractors, we recommend obtaining formal advice. But that does not mean simply getting a letter from your accountant or lawyer that rubber stamps your treatment of anyone as a contractor. It must be independent and objective.

Nexia can provide advice on how to correctly apply the law and determine whether a person is an employee or contractor. If the conclusion is that they are an employee, well, you’ll know where you stand. If the conclusion is that they are a contractor, you’ll have genuine support for that position, as the difference in withholding, superannuation and workers’ compensation consequences is significant. It’s also a cost-effective insurance policy against losing the deduction in the event of the ATO disagreeing.

At Nexia, we can give you peace of mind in managing a significant risk in your business that has now only got riskier.

From darkness, to light.