The Organisation for Economic Co-operation and Development (OECD) has been involved for a number of years in developing measures designed to prevent Base Erosion and Profit Shifting (BEPS). In order to effectively target BEPS, governments need to be able to change their international laws rapidly. Under the existing tax treaty network, it can take a number of years for a tax treaty to be updated and ratified by both countries. These time constraints can be overcome through the use of a Multilateral Instrument (MLI).

The MLI is a multilateral treaty that enables jurisdictions to swiftly modify their bilateral tax treaties to implement measures designed to better address multinational tax avoidance.

Who does it apply to?

Jurisdictions that sign the MLI are required to identify to which treaty partners they want the MLI to apply. The tax treaties covered by the MLI are called Covered Tax Agreements (CTAs).

Both treaty partners need to identify their bilateral treaty as a CTA in order for that treaty to be modified by the MLI. For the avoidance of doubt, the MLI will not apply where only one jurisdiction identifies a bilateral treaty as a CTA.

What applies in a CTA?

There are some MLI articles which the OECD has deemed mandatory but the majority of articles are optional. The optional articles can be applied as is, or with modifications or reservations. This provides flexibility that allows jurisdictions to tailor their adoption to fit their treaty network and national preferences. If there is a bilateral match, the MLI will modify but not directly amend the chosen tax treaty clauses. The remaining parts of the tax treaty will not be changed.

What is Australia’s approach?

On 26 September 2018, Australia ratified the MLI into its domestic law. The MLI will enter into force for Australia on 1 January 2019. As stated above, the extent to which the MLI will modify Australia’s bilateral tax treaties will depend on the final adoption positions taken by its treaty partners.

The date of entry into effect for each of Australia’s CTAs depends on the actions of its treaty partners. Each treaty partner would be expected to ratify the MLI within their domestic law and lodge the relevant notifications with the OECD.

Subject to these processes, it is expected that the earliest the MLI can take effect in Australia is for:

- withholding taxes, on income derived on or after 1 January 2019

- all other taxes, for income years starting on or after 1 July 2019

- dispute resolution, after the MLI enters into force for each of the parties.

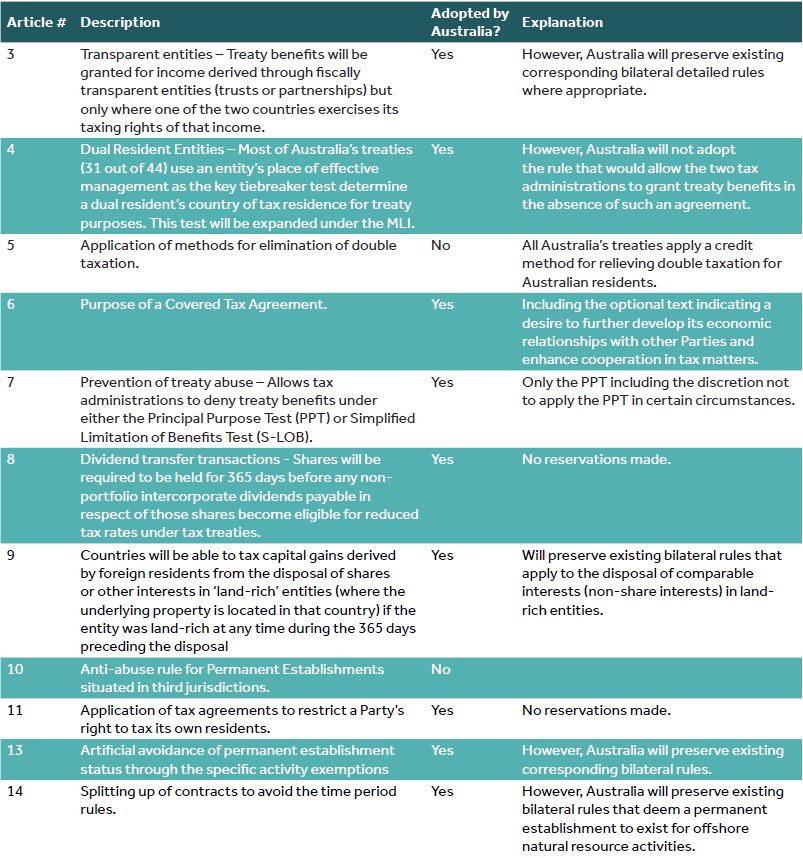

Some of Australia’s key adoption provisions in respect of the MLI have been reproduced below:

What does this mean for doing business in Australia?

As there are still a number of options that need to be decided and ratified by our treaty partners, it is too early to comment on the impact that these changes will have on doing business in Australia. What we can see from the articles adopted by the Australian Tax Office (ATO) is that the ATO is seeking to implement the majority of OECD’s suggested measures and is focusing on the tax structuring that occurs into and out of Australia. This can be seen in particular in the following articles.

Tax structures which seek to benefit from the different treatment of certain legal entities in different jurisdictions are specifically targeted in Article 3. Article 3 aims to remove the double non-taxation benefits currently possible where an entity such as an LLP is favourably treated as a company in one jurisdiction and a partnership in another jurisdiction.

Another type of structure which is affected by Australia’s adoption of the MLI is the use of holding companies which are inserted into a group structure for the principal purpose of obtaining a treaty benefit such as preferential withholding tax rates. This practice, known as ‘treaty shopping’ would not be possible under Article 4 of a CTA.

Finally, Articles 4, 13 and 14 are designed to increase the amount of companies which may be considered to have a taxable presence in Australia and care needs to be taken where the activities of taxpayers would have escaped the Australian tax net under existing tax treaties but may now be caught under the new articles.

Conclusion

Whilst the impact of the MLI is yet to be seen, it does provide a strong indication that the ATO is taking a hard line on profit shifting and will use the MLI, as well as a number of domestic anti-avoidance measures, to see that multinationals operating in Australia pay tax in Australia. In light of Australia’s new rules we recommend revisiting your clients’ structures.